Register to continue reading for free

Retail Flash: end-2025 insights from key footwear markets

Explore the main retail dynamics across France, Germany, Japan, the Netherlands, the UK, the US and Spain, including end-2025 insights and early-2026 signals, highlighting online outperformance in France and Spain, persistent footwear weakness in Germany, and import-cost pressure in Japan and the US

France

French retail activity remained largely flat through 2025, with total sales broadly unchanged from the previous year, as retailers reported weaker in-store footfall and smaller average basket sizes despite heavier discounting.

Online sales continued to outperform, rising by 4.8% year over year. In contrast, footwear sales declined in 2025, averaging a 2.5% contraction in a market where low-price strategies and the growing presence of Asian players were seen as widening the gap between entry-level prices and the market average.

Inflation trended down steadily, ending the year well below the 2% benchmark, with subdued price growth mirrored in clothing and footwear despite the latter’s greater volatility.

Overall, footwear import growth was minimal, with sharp month-to-month swings suggesting uncertain demand and more conservative buying by retailers to limit unsold stock.

Political conditions may have stabilised somewhat following the approval of the 2026 budget. Still, higher taxes and a fragile economic backdrop leave the outlook for a clear rebound uncertain, with the sector viewing seasonal sales as an important lever to rebuild store traffic and clear inventory.

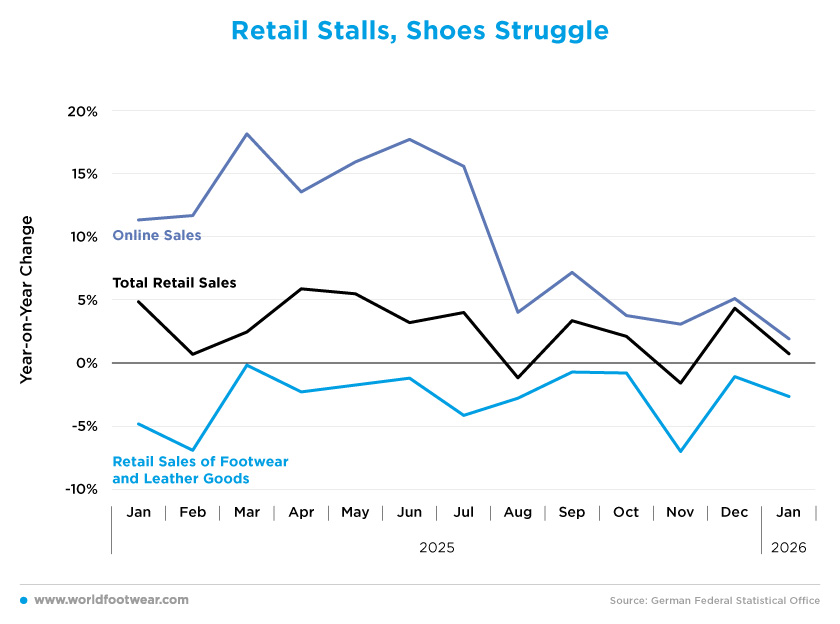

Germany

Germany’s footwear and leather goods retail segment remained under sustained pressure in 2025, with sales declining year-on-year throughout the period and still negative at the start of 2026.

Industry strain has been reflected in company distress and continued store closures, as weaker footfall and the longer-term shift towards online shopping intensified competition for traditional retailers.

Online retail remained the clearest source of growth, although the pace moderated as the year progressed, and large marketplaces continued to gain share in fashion and footwear.

Consumer sentiment stayed weak despite some improvement, while headline inflation hovered close to the central bank’s target. Footwear prices, however, were more volatile and dipped into deflation at points, consistent with heavier discounting to stimulate demand.

In contrast to weak sell-through, footwear import values rose strongly for much of 2025, with notable increases from Asian hubs and European producers.

The gap between robust import flows and fragile domestic conditions may partly reflect Germany’s role as a regional distribution centre. At the same time, industry representatives expect a broadly stable sales outlook in 2026 amid continued policy and geopolitical uncertainty.

Japan

Japan entered 2026 with headline inflation easing, a gradual tightening of monetary policy, and only a fragile improvement in consumer sentiment.

Inflation fell sharply over 2025 and continued to moderate into early 2026, aided by stabilising food prices and government support measures, even as policymakers remained alert to renewed pressures from energy costs and currency weakness.

Consumer confidence recovered from a low point in spring 2025 and improved through early 2026, but remained vulnerable to shocks and rising living costs, reinforcing a cautious tone in household demand.

Within that backdrop, fashion-related trends diverged from the wider disinflation story. Clothing prices held near a relatively stable pace through 2025, while footwear inflation climbed mid-year before easing to around the low single digits in early 2026.

Commercial sales remained positive for the economy as a whole, but apparel and accessories, including footwear, contracted throughout the period.

Footwear import values rose throughout most of 2025 even as volumes fluctuated, suggesting that the weak yen raised import costs without necessarily bringing in significantly more pairs.

The Japanese currency remained soft against the dollar for much of the year, contributing to higher import bills and adding to pressure on both companies and consumers.

Netherlands

Over the full year, overall retail turnover grew steadily within a narrow band, averaging 3.1%. Online retail outpaced the wider sector, expanding at an annual average of 6.5% in total retail, though growth slowed in the second half of the year.

Fashion retail, combining clothing and footwear, remained more irregular, with footwear showing the sharpest month-to-month swings. Turnover averaged 2.1% across 2025 and decreased slightly in December.

Inflation moderated, decreasing to 2.7% in December 2025, while footwear prices were notably volatile and, on average, slightly lower over the year.

Entering 2026, consumer sentiment indicators diverged. Confidence remained negative and weakened again after earlier improvements, while retail confidence stayed positive.

Against this mixed backdrop, footwear import growth in value terms trended down through 2025 and turned negative in early autumn, adding uncertainty to the outlook.

United Kingdom

UK sales of textiles, clothing and footwear strengthened across 2025, outpacing total retail and ending the year with notable momentum into early 2026. Online sales grew as well, and fashion-related e-commerce rose more sharply at key points.

Despite rising turnover, average consumer spending on footwear remained broadly flat, suggesting growth was driven more by transaction volumes or the number of active shoppers than by higher spend per customer, consistent with households staying selective amid ongoing uncertainty.

Price dynamics underscored the pressure on margins in non-food retail. While headline inflation remained elevated through much of 2025, footwear prices stayed in deflation throughout the year, indicating persistent discounting.

Footwear import values were volatile, swinging between sharp rises and declines, which suggests retailers are adjusting orders rapidly in response to short-term changes in demand and adopting more reactive inventory management.

Cost pressures, tax uncertainty and cautious consumer behaviour continue to shape investment and stock decisions across the sector.

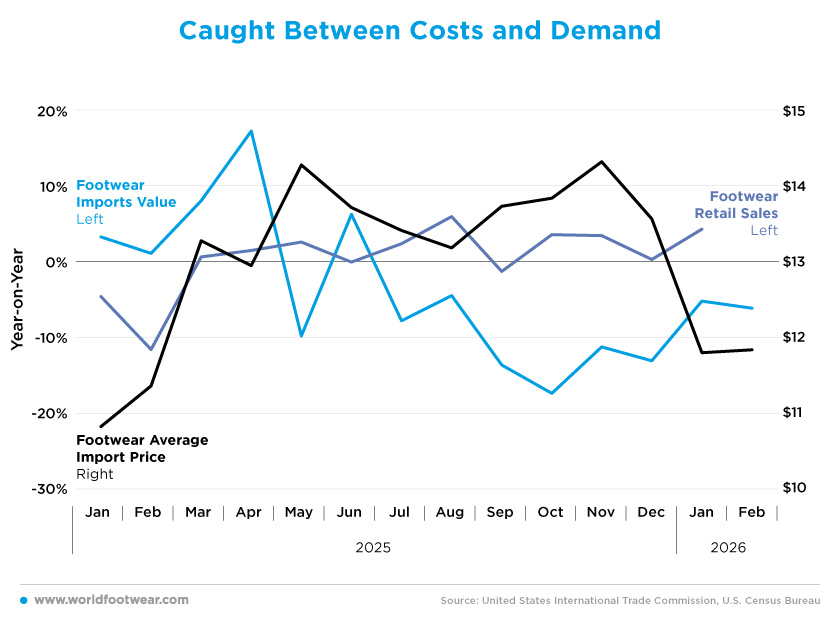

United States

US retail sales remained positive throughout 2025. Within fashion, however, performance diverged. Clothing and accessories generally outpaced the wider retail market, while footwear was more irregular, swinging between contraction and growth before strengthening towards the end of 2025 and into early 2026.

Online retail continued to expand, but its share of overall sales appeared broadly stable for most of the year and rose mainly during the holiday period.

Macroeconomic signals were more mixed. Inflation eased overall, while the Federal Reserve began cutting interest rates after holding policy steady for much of the year, reflecting concern about the wider outlook as consumer sentiment weakened sharply before a modest early-2026 recovery.

In footwear, import values shifted from growth to sustained decline from late spring onwards, mirroring weakness in footwear store sales during the same period. At the same time, average import prices rose markedly through much of the year, suggesting cost pressures linked to sourcing disruption and trade policy uncertainty.

The combination of higher import costs and softer retail demand points to a squeeze on the segment, with part of the burden absorbed through higher prices and part through lower volumes.

Spain

Spain ended 2025 with strong headline economic growth of 2.8%, but the fashion retail segment failed to benefit from broader momentum.

Fashion sales fell on average over the year, and the end-of-year trading period underperformed expectations, with industry representatives warning that demand has not recovered sustainably.

Early 2026 indicators remained subdued, with only a marginal uptick in fashion sales. This contrasted with the wider retail market, which continued to expand briskly through 2025, supported primarily by e-commerce. Large operators with strong omnichannel reach, including Inditex, continued to record sales growth, suggesting resilience at the top end of the market.

Headline inflation averaged 2.7% in 2025, while clothing and footwear prices moved in the opposite direction, indicating limited scope to pass on cost increases to consumers. The price gap widened at the start of 2026, when fashion prices saw an unusually sharp monthly fall, with women’s footwear experiencing a larger adjustment than men’s.

Despite signs of stabilising consumer sentiment and strong credit growth, households remained cautious, and sector conditions continued to diverge from the wider economy.

Against this backdrop, footwear imports rose strongly through 2025 before easing later in the year, a pattern that may be linked not only to domestic demand but also to increased importing for onward re-export.