Register to continue reading for free

Japan Retail: fashion falls out of step with the market

Although inflation is cooling and the macroeconomic situation in Japan is stabilising, consumer confidence remains fragile. Against this backdrop, the fashion industry appears to have fallen out of step, with clothing and footwear prices remaining high while demand continues to weaken. This is evident in the continued decline in apparel and textile sales, contrasting with the resilience of the broader retail sector. At the same time, the weak yen is inflating import costs, forcing footwear companies to pay more without achieving significant increases in sales volume

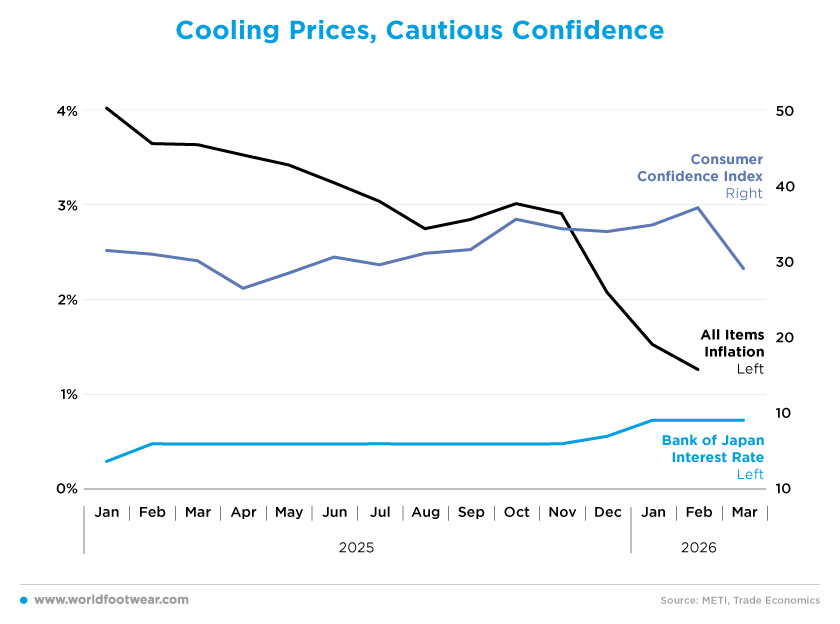

Cooling Prices, Cautious Confidence

The macroeconomic environment in Japan in 2025 and early 2026 has been characterised by easing inflation, a gradual shift in monetary policy, and a fragile recovery in consumer sentiment.Inflation declined steadily throughout last year, falling from 4.0% in January to 2.1% by December, and easing further to 1.3% in February 2026. Recent data suggests that this slowdown was supported by stabilising food prices and government subsidies, which helped shield consumers from rising energy costs, even as underlying inflation remained firmer than the headline figure implied (cnbc.com). However, the available data does not yet reflect the impact of the war in the Middle East.

At the same time, the Bank of Japan (BoJ) began moving from ultra-loose monetary conditions. Having kept its policy rate broadly stable at around 0.48% for most of 2025, the Bank raised rates to 0.56% in December and to 0.73% in early 2026. This tightening path is consistent with BoJ’s view that inflation is moving closer to its 2% target. Nevertheless, policymakers remain alert to the risk that a weak yen and higher energy costs could reignite price pressures (reuters.com).

Although still subdued, consumer confidence showed signs of gradual improvement. After declining to a low of 31.2 in April, the index recovered steadily in the second half of the year, reaching 38.5 in October, and rising further to 39.7 by February 2026. Even so, sentiment remained fragile, as households continued to worry about living costs, inflation, and the broader economic outlook. This fragility was particularly evident in March 2026, when confidence fell again due to higher fuel prices and geopolitical tensions (investinglive.com).

The combination of falling inflation, rising interest rates and improving – albeit still relatively weak – consumer sentiment suggests that Japan is entering a transitional phase, in which macroeconomic conditions are stabilising, but household demand remains cautious.

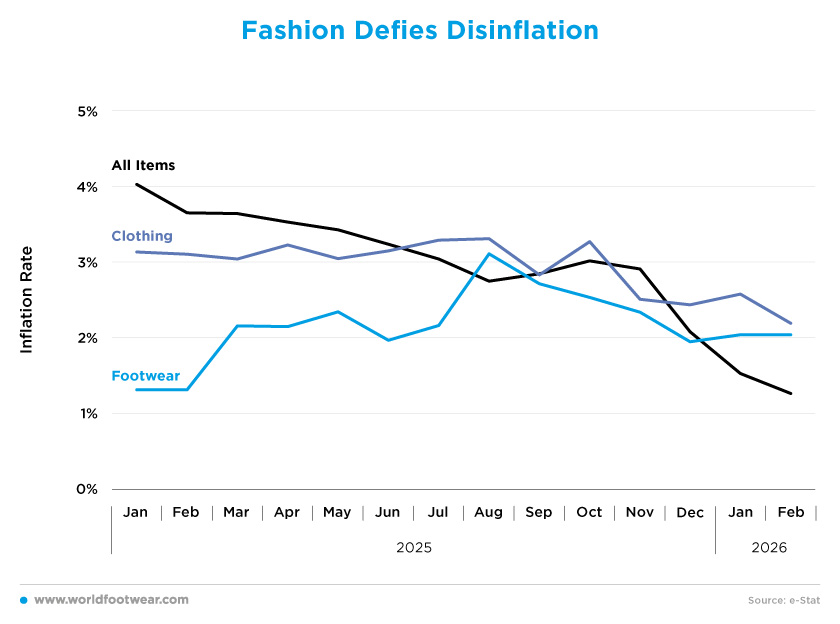

Fashion Defies Disinflation

Inflation dynamics in Japan reveal a clear divergence between overall price trends and those observed in the fashion sector. While headline inflation declined steadily over the course of 2025, prices of clothing and footwear remained comparatively more stable.As previously mentioned, all-items inflation fell from 4.0% in January to 2.1% in December, continuing to ease to 1.3% by February 2026. This downward trajectory reflects a general cooling in price pressures across the economy, which is consistent with the current macroeconomic situation.

In contrast, clothing prices showed a much more stable pattern. Throughout 2025, clothing inflation remained close to the 3% mark, fluctuating within a relatively narrow range between of 2.5% to 3.3%. While overall inflation declined, clothing prices did not follow the same downward trend, only moderating slightly towards the end of the year and into early 2026.

Footwear inflation followed a somewhat different trajectory. Starting from a level of around 1.3% at the beginning of the year, it gradually increased over the first half of 2025, peaking at 3.1% in August. Over the subsequent months, footwear inflation eased again, stabilising at around 2.0% in early 2026.

This divergence reflects the underlying structure of price pressures in Japan, where inflation has been driven in part by cost factors such as imported inputs and energy. Some categories, particularly those more exposed to global supply chains, have experienced more persistent price increases (japantimes.co.jp).

As the Japanese footwear market is heavily dependent on imports, the sector is especially vulnerable to these price pressures, diverging from the general economic trend.

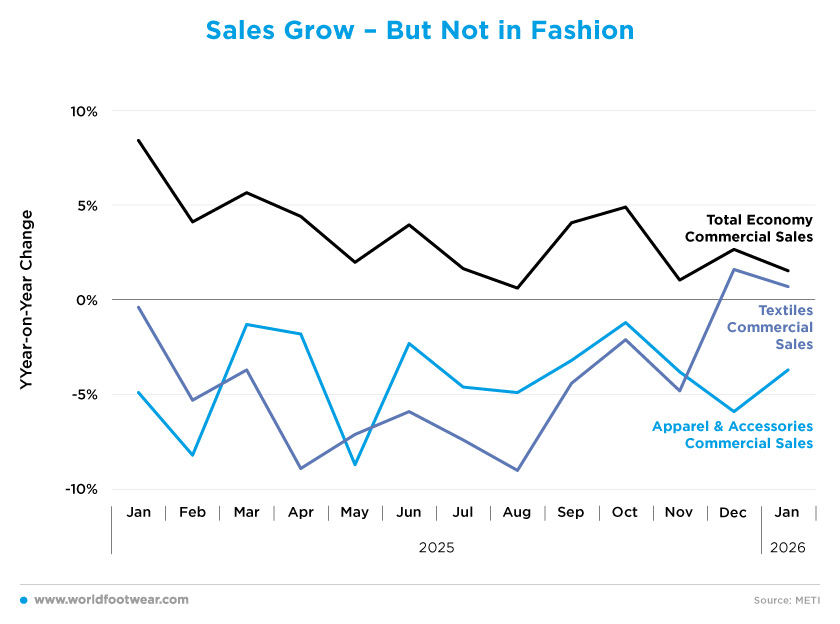

Sales Grow – But Not in Fashion

Commercial sales data in Japan highlights a clear discrepancy between the overall state of the economy and the performance of the fashion-related sectors. Although total commercial sales remained consistently positive throughout 2025, there were sustained contractions in both apparel and textiles.Total economy commercial sales grew strongly at the beginning of the year, increasing by 8.4% in January, before moderating in the following months. Despite this slowdown, positive growth was maintained throughout the year, fluctuating between 0.6% and 5.7%, and reaching 1.5% in January 2026. This suggests that, even as momentum softened over time, overall economic activity has remained relatively resilient.

Overall, this reflects broader weakness in consumer demand and retail activity in Japan. Higher living costs and economic uncertainty have led to more cautious spending behaviour, particularly in discretionary categories such as clothing and textiles. Recent data indicates softening retail demand and declining sales momentum towards the end of 2025, which reinforces this trend (finance.yahoo.com).

Apparel and accessories (including footwear) sales were negative throughout the entire period. Following a 4.9% decline in January, the sector experienced a further contraction, with losses deepening to 8.7% in May and remaining consistently negative for the rest of the year. Although the pace of decline moderated slightly in some months, sales never returned to positive territory, finishing at -3.7% in January 2026.

The textiles segment performed even more poorly. Sales were negative in almost every month of 2025, with declines of up to 9.0% in August. Although there were brief signs of stabilisation towards the end of the year, including slight positive growth in December (1.6%) and January 2026 (0.7%), the overall trend remained firmly negative.

This contrast between positive overall commercial sales and the decline of the fashion-related sectors suggests Japan’s growth is being driven by other areas of the economy.

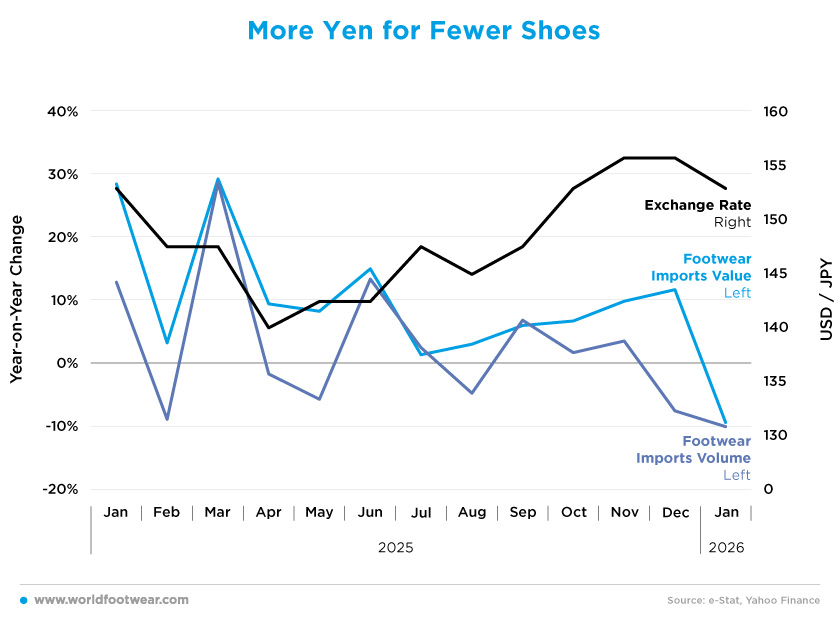

More Yen for Fewer Shoes

The value of footwear imports into Japan increased for most of 2025, but the volume showed a much more uneven pattern.Import values rose sharply at the start of the year, increasing by 28.4% in January and 29.2% in March, and remained positive throughout the year. Even during the second half of the year, when growth moderated, import values still expanded by between 1.5% and 11.7%. It was only in January 2026 that import values turned negative, falling by 9.2%.

Import volumes, however, tell a more mixed story. While there were significant gains in some months, such as January, March, June and September, several months saw declines, including February, May, August and December. This suggests that the rise in import values cannot be explained solely by higher quantities, and that price or currency effects were likely an important factor.

The exchange rate supports this interpretation. Throughout the period, the yen remained weak against the dollar throughout the period, fluctuating mostly between 143 and 156 yen per dollar. After strengthening briefly in April, the currency weakened again in the second half of the year, reaching 156.3 yen per dollar in both November and December. This made imported goods became more expensive in yen terms, thereby raising the cost of foreign-sourced footwear, even though import volumes did not increase significantly.

The gap between import values and volumes suggests that Japan’s footwear trade was influenced not only by demand, but also by the effects of exchange rates. In practical terms, importers often paid more in yen without necessarily bringing in substantially more products.

This dynamic is consistent with broader concerns about the state of the Japan’s economy, where the weak yen has continued to push up import costs and add to inflationary pressures. According to Reuters, policymakers and analysts have repeatedly identified currency weakness as a factor that raises the cost of imported goods and squeezes both firms and households (reuters.com).