Register to continue reading for free

France Retail: uncertainty hangs over the year ahead

The French retail sector remained largely stagnant in 2025. Subdued sales, declining consumer confidence and cautious household spending negatively impacted footfall and average basket sizes in physical stores. While e-commerce continued to grow, the footwear sector experienced falling sales, negative sentiment and limited inflationary support. Data on imports also suggests that retailers have adopted more cautious inventory management strategies. Even the approval of the new Budget does not appear to lift the cloud of uncertainty hanging over the year ahead

Online Leads, Footwear Lags

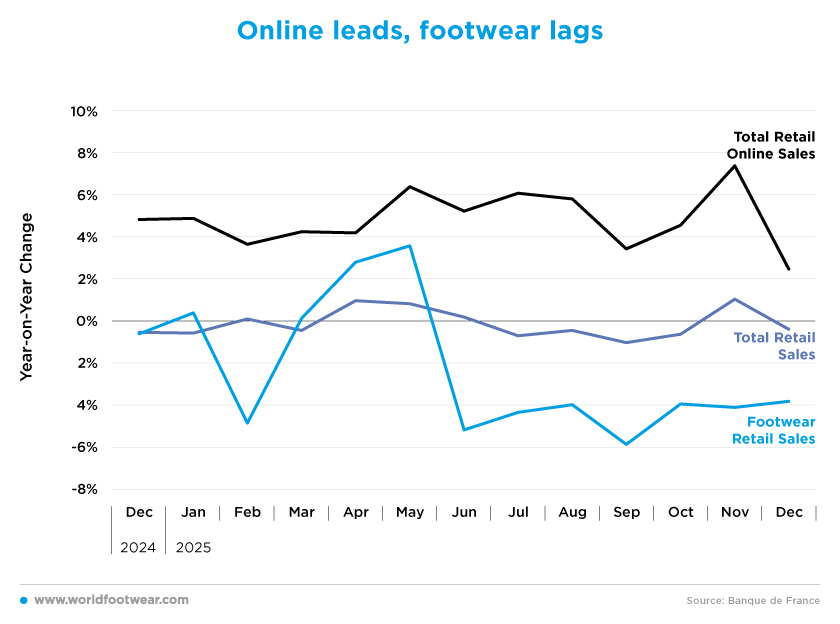

The French retail sector showed weak performance throughout 2025. With relatively low volatility – fluctuating within a narrow range of around ±1% – total retail sales remained broadly stagnant compared with the previous year, with an average change of -0.1% recorded.Evidence from retailers’ reports support this trend: more than half of them reported a decline in footfall at physical points of sale, while 44% observed a reduction in average basket size. Taken together, these indicators suggest increased household caution, despite aggressive markdowns at the start of the autumn–winter season (fashionunited.fr).

E-commerce performed more strongly in 2025, with total online retail sales increasing by 4.8% year-on-year. Growth peaked in November at 7.4%, reaching a low of 2.4% in December. This performance reflects the ongoing digital transition, which continues to put pressure on physical retail.

According to the Fédération du e-commerce et de la vente à distance (Fevad), total e-commerce turnover approached 200 billion euros, representing nearly 7% of GDP, despite the highly uncertain political and economic environment. The volume of transactions also increased by 10% to reach 3.2 billion – the equivalent to more than 100 orders per second in France. Marc Lolivier, General Delegate of Fevad, noted that this constitutes an “important symbolic milestone” for the sector (france24.com).

By contrast, the footwear segment contracted over the course of 2025, despite temporary increases in January (2.8%) and May (3.6%). On average, sales declined by 2.5% year-on-year. This may be partly explained by the rise in online sales and the growing prevalence of low-price strategies in the sector, reinforced by the strong presence of Asian players.

As highlighted by Gildas Minvielle, Director of the IFM Economic Observatory, “we’re seeing a widening gap between very low prices and the market average,” which is also affecting consumers’ price perceptions. At the same time, while fashion remains the leading category in online sales, it is also the segment experiencing the sharpest decline overall, according to Fevad’s 2025 report (uk.fashionnetwork.com).

Inflation in Sync but Below Target

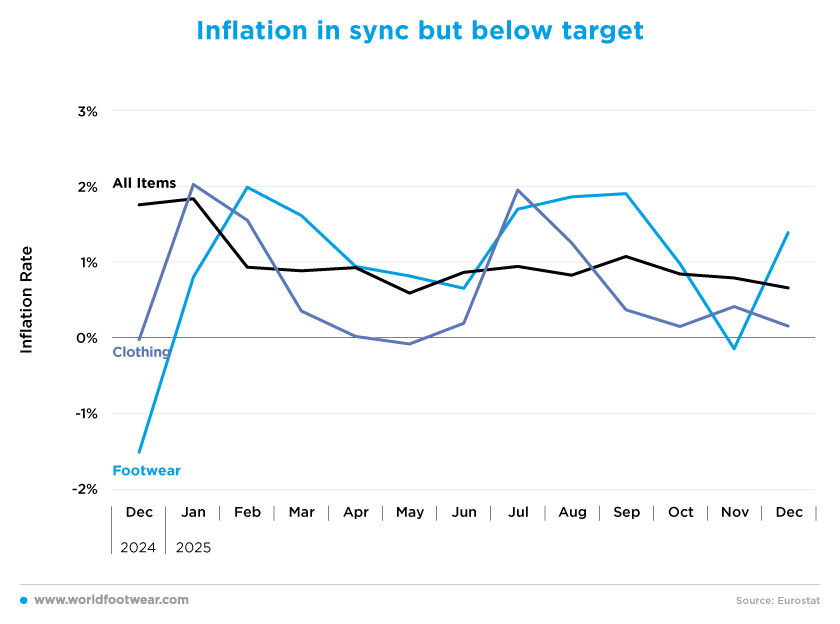

Inflation (all items) followed a stable and gradual downward trend throughout 2025, declining from 1.8% in January to 0.7% in December, which resulted in an annual average of 0.9%. This points to a relatively subdued economic environment, consistent with GDP growth of below 1%. Nevertheless, economic activity proved more resilient than many forecasters had anticipated, despite prolonged political uncertainty and a deeply divided parliament weighing on household and business sentiment (reuters.com).In the fashion sector, price variations broadly mirrored aggregate developments. On average, clothing prices increased by 0.7% in 2025, while footwear recorded slightly higher inflation at 1.2%, albeit with greater volatility throughout the year. In line with overall inflation, both segments showed signs of slowing price growth. However, this may be a cause for concern, as inflation across these categories remains below the 2% benchmark, and further disinflation could weigh on business conditions in the sector.

Looking ahead, the approval of the 2026 budget in February may signal a degree of renewed political stability. Finance Minister Roland Lescure stated that “we’re off to a good start in 2026” and expressed hope that growth would reach at least 1%. Nevertheless, prospects for a strong rebound remain limited. According to ING Group economist Charlotte de Montpellier, the budget “remains unfavourable to businesses”, with higher taxes likely to weigh on investment and job creation, while a strong euro could continue to act as a drag on exports (reuters.com).

Gloom Weighs on Shoes

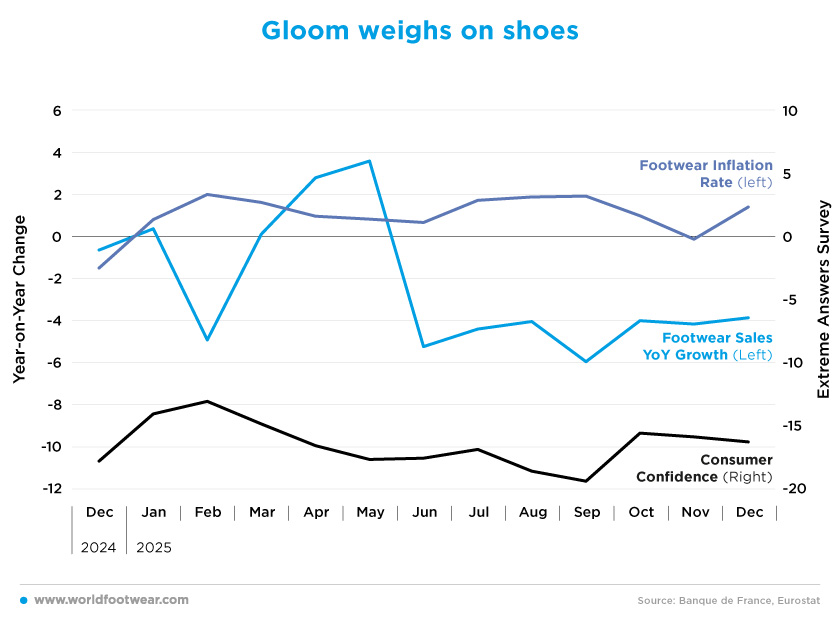

Combining the previous analyses of sales and inflation with developments in consumer confidence provides a clearer picture of the performance of the footwear sector.Throughout 2025, consumers consistently reported negative expectations, likely contributing to more cautious purchasing behaviour, as reflected in both reduced consumption and a shift towards lower-priced alternatives. This, in turn, helps explain the combination of weak sales dynamics and subdued inflation in the sector.

The consumer confidence indicator, part of the European Commission’s economic sentiment surveys, measures the balance between positive and negative responses, expressed in percentage points (pp). In 2025, confidence remained firmly in negative territory, peaking at -13 pp in February and reaching a low of -19.3 pp in September, before declining further to -16.2 pp by the end of the year.

Overall, these developments suggest that consumer sentiment in France remains weak. While potential political stabilisation could support a recovery in confidence, the fiscal consolidation set out in the 2026 budget – in the context of a still-fragile economic environment – could continue to weigh on households and businesses alike. As such, the outlook for 2026 remains uncertain.

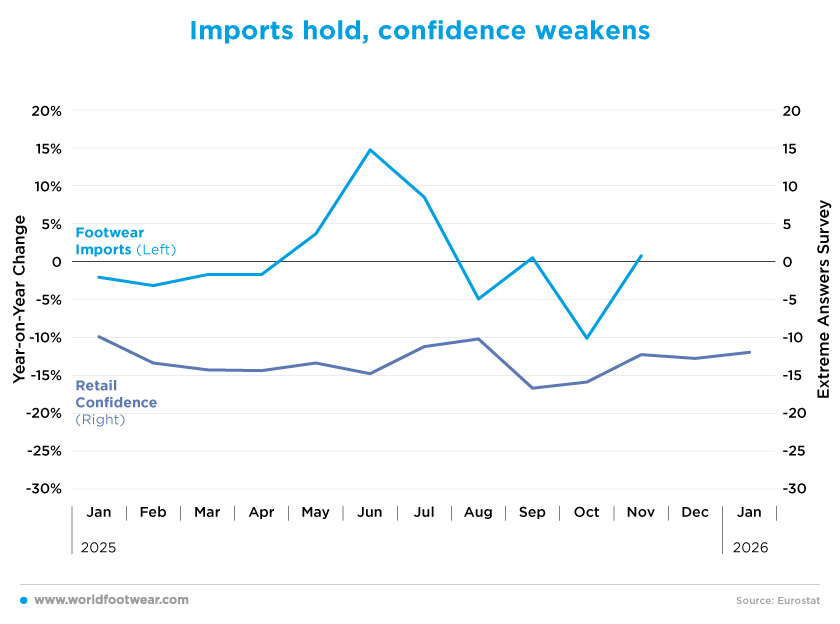

Imports Hold, Confidence Weakens

As expected in the context of weak retail sales, retailer confidence remained subdued throughout 2025. Sharing similar concerns to those of consumers, the broader economic environment in France was not conducive to strong business activity. As a result, retail confidence stayed firmly in negative territory, starting at -10 pp in January, falling to a low of -17 pp in September, and recovering slightly to -12 pp by the end of the year.Against this backdrop, footwear imports also showed weak dynamics last year, with growth of just 0.4% year-on-year between January and November. As is typical for the sector, volatility remained high, with growth peaking at 15% in June and dropping to -10% in October. At the same time, retailers appear to be adopting more cautious inventory management strategies, purchasing smaller volumes at the start of the season to limit unsold stock, thereby reducing supply during sales periods (fashionunited.fr).

Following such a stagnant year, and with an uncertain outlook for 2026, any opportunity to support business activity is particularly important. As Yohann Petiot, Managing Director of the Alliance du Commerce, noted, “In this context, the winter sales are more important than ever for the sector”. “They must enable retailers to rebuild footfall in stores, support business activity, and clear stock within a clear and regulated framework for the benefit of both consumers and retailers” (fashionunited.fr).