Register to continue reading for free

Germany Retail: Footwear under pressure amid clouded outlook

Germany’s footwear and leather goods sector remained under pressure in 2025, with weak consumer and retail confidence, falling sales, and substantial discounts weighing on the market, despite the expansion of the online channel and a significant increase in footwear imports. Looking ahead, industry representatives appear to anticipate cautious stabilisation rather than a clear rebound. While e-commerce and Germany’s role as a regional hub offer some support, weak domestic demand and persistent uncertainty continue to cloud the outlook

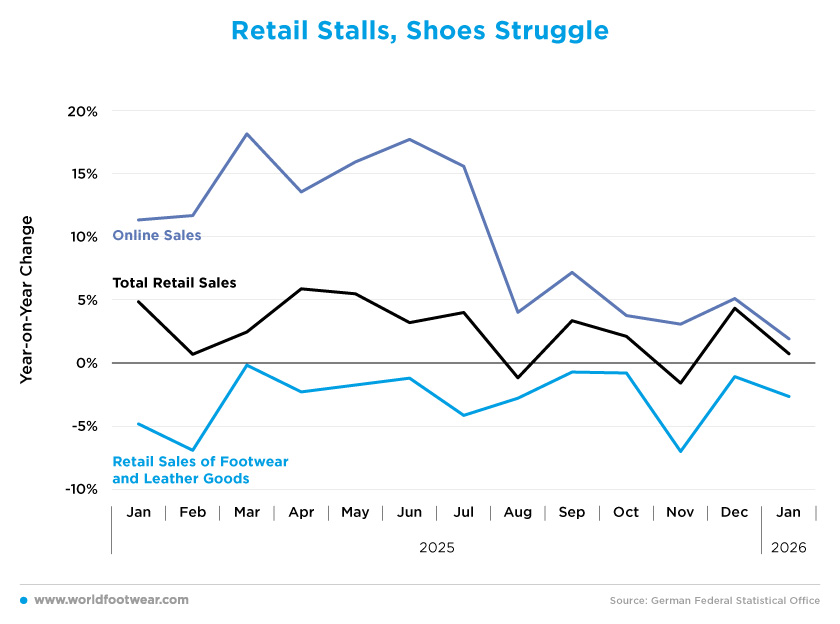

Retail Stalls, Shoes Struggle

The footwear and leather goods sector continued to struggle in Germany in 2025, with retail sales in the segment remaining negative throughout the year.After a sharp drop at the start of the year, with sales down by 4.8% year-on-year in January and by 6.9% in February, the contraction briefly moderated in March, before slipping back again in the subsequent months. Despite some smaller declines in the spring and early summer, the sector never returned to positive territory. By November, footwear sales had fallen by as much as 7.0% compared to the same month a year earlier. Even at the start of 2026, the sector remained under pressure, with sales still down by 2.6% year-on-year in January.

The difficulties facing the footwear segment come at a time when Germany’s wider economy remains fragile, with businesses still grappling with weak domestic demand and high operating costs. Several footwear companies have experienced financial distress, including the wholesaler Pölking, which has filed for insolvency again after struggling with weakening sales and mounting expenses. Smaller retailers have also continued to close stores across the country amid declining footfall and structural shifts towards online shopping (shoeintelligence.com).

This contrasts with the broader retail sector, which saw modest but mostly consistent growth throughout much of the year. Total retail sales rose by 4.8% in January and remained generally positive during the first half of 2025, with April and May posting increases of around 6% and 5.5%, respectively. However, momentum weakened in the second half of the year, with retail sales turning briefly negative in August and November, before ending the year with a 4.3% increase in December. Sales stalled in the first month of 2026, with a year-on-year change of 0.7%.

Online retail, meanwhile, continued to outperform physical stores for most of the year. Online sales began 2025 with strong double-digit growth, reaching 11.3% in January and peaking at over 18% in March. Although this momentum gradually slowed as the year progressed, growth remained positive throughout the year, ending at 5.1% in December and moderating further to 1.9% in January 2026.

Germany’s e-commerce sector has been one of the few bright spots in the country’s retail landscape, having returned to growth after several turbulent years marked by inflation and weak consumer confidence. Online fashion and footwear sales have performed particularly well, while large marketplaces have continued to gain ground. Platforms such as Temu, Shein and AliExpress now account for a growing share of online orders (shoeintelligence.com).

This divergence suggests that, although overall consumer spending has remained cautious, digital channels are capturing an increasingly larger share of retail demand, thereby intensifying the competitive pressure on traditional footwear retailers.

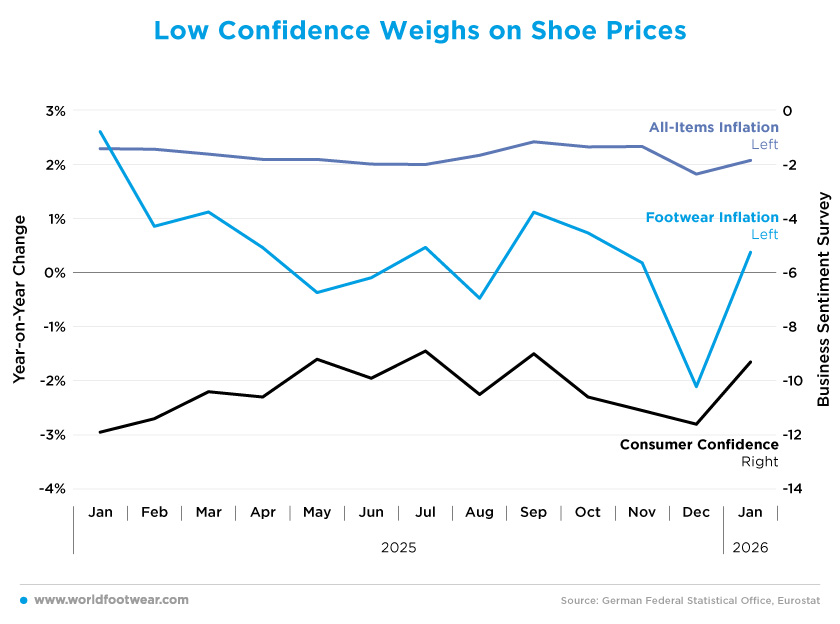

Low Confidence Weighs on Shoe Prices

Despite some gradual improvement, consumer sentiment in Germany remained weak throughout 2025. The consumer confidence indicator stayed negative during the entire year, fluctuating between -11.9 in January and -11.6 in December, before improving slightly to -9.3 in January 2026. The indicator briefly approached the -9 level during the summer months, suggesting a temporary improvement in sentiment. However, the recovery proved fragile, with confidence slipping again towards the end of the year.

German consumer confidence remains subdued as households continue to face economic uncertainty, despite some macroeconomic indicators showing tentative signs of stabilisation. Surveys indicate that consumers are still being cautious about how they spend money, with geopolitical tensions and financial pressures contributing to a general sense of pessimism among households. “Even though the economy appears to be recovering slightly, consumers remain sceptical,” said Rolf Buerkl, head of consumer climate at Nuremberg Institute for Market Decisions (wsj.com).

Inflation developments have been comparatively stable. Overall, consumer price inflation hovered close to the European Central Bank’s target throughout the year, averaging around 2.2%. After starting the year at 2.3%, inflation eased gradually to 2.0% in by the middle of the year, before rising again to around 2.4% in September. Towards the end of the year, inflation moderated again, reaching 1.8% in December before moving back to 2.1% in January 2026.

“Inflation in Germany remains in the green”, said Ulrich Kater, chief economist at DekaBank. “Price increases have been dampened in recent months by lower energy prices and a strong euro against the US. dollar” (reuters.com). However, the recent conflict in the Middle East could drastically change this situation.

The pattern of footwear prices differed from that of headline inflation. After starting the year with relatively strong price growth of 2.6% in January, footwear inflation weakened considerably in the following months and even turned negative in May and August. Prices recovered briefly in September and October, but then dropped sharply again in December, reaching -2.1% year-on-year, before returning to modest growth in January 2026.

This volatility in footwear prices most likely reflects retailers’ attempts to stimulate demand through discounting amid weak sales conditions, suggesting that retailers have used pricing strategies as a tool to maintain turnover in a difficult retail environment.

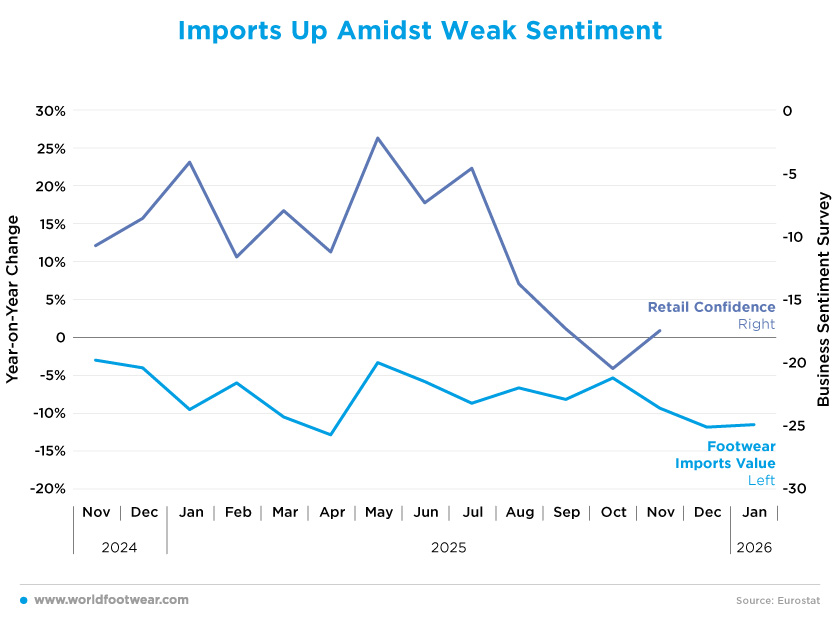

Imports Up Amidst Weak Sentiment

Germany’s footwear imports showed strong growth during most of 2025, despite the weakness observed in retail sales. Import values recorded double-digit increases at the beginning of the year, rising by 23% year-on-year in January and remaining above 10% throughout the spring months. Growth remained solid until the beginning of summer, peaking at 26% in May, before slowing down gradually during the second half of the year. Growth nearly stalled by September, and imports briefly turned negative in October, before returning to modest growth in November.In 2025, imports reached more than 700 million pairs, with particularly strong growth from Asian manufacturing hubs such as Vietnam and Indonesia. China remained the largest supplier to the German market, accounting for more than 40% of total imports. Meanwhile, Germany’s footwear imports from key European producers, including Italy, Portugal and Spain, increased significantly (5.2%, 16.7% and 35%, respectively) (ostechnik.de).

By contrast, retail confidence remained deeply negative throughout the period. The indicator fluctuated between approximately -20 and -25 points in 2025, reaching particularly low levels in April and again towards the end of the year. Although sentiment improved slightly at times during the summer months, the index never returned to positive territory, highlighting the ongoing caution among retailers.

Nevertheless, industry representatives expect conditions to stabilise in the coming months. According to the German Federal Association of the Footwear and Leather Goods Industry (HDS/L), many companies expect sales to remain broadly stable in 2026, although domestic demand and economic policy and geopolitical uncertainty continue to pose risks to the sector (ostechnik.de).

It should be noted that the discrepancy between robust import flows and weak retail confidence may be partly due to Germany’s role as a major distribution hub within the European footwear market – this means that imported products are not only for people in Germany to buy, but also to sell to other countries nearby.