Register to continue reading for free

UK Retail: fashion retail grows, but caution persists

Sales in the UK’s textile, clothing, and footwear (TCF) sector recovered in 2025, exceeding total retail figures despite periods of volatility. However, this recovery was driven more by increased transaction volumes than by higher consumer spending, with expenditure on footwear remaining largely unchanged and prices declining amid persistent discounts. At the same time, volatile yet growing online sales and increasingly responsive import patterns suggest that the sector is trying to adapt quickly to uncertain demand

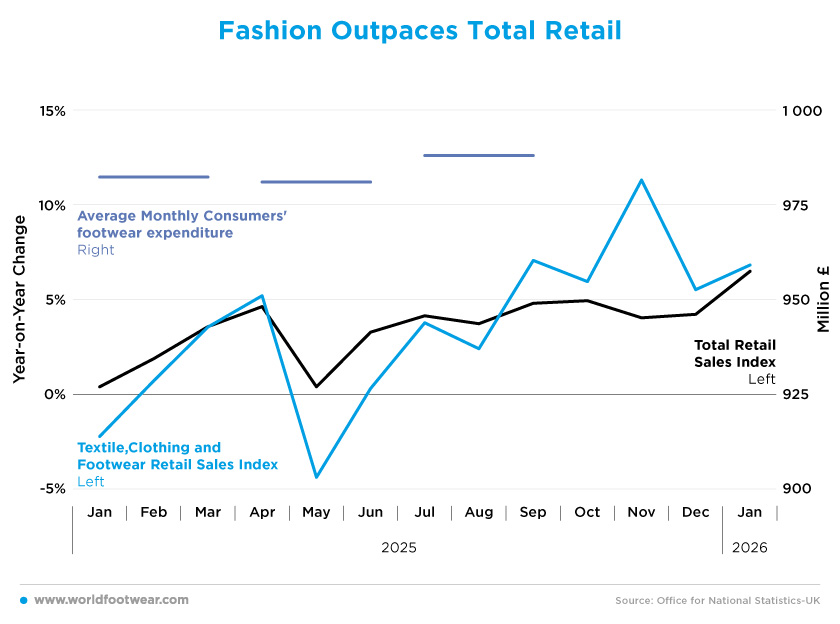

Fashion Outpaces Total Retail

Textile, clothing, and footwear (TCF) sales showed a strong recovery in the UK throughout 2025, despite some volatility during the year.

After contracting by 2.2% in January, TCF sales rebounded quickly, turning positive in February and reaching consistent growth rates during the spring. Although May saw another decline of 4.4%, the sector regained momentum in the following months, with sales increasing steadily throughout the summer and peaking at 7.1% in September. Growth remained robust in the final quarter, with a standout increase of 11.3% in November, before moderating slightly to 5.5% in December, and continuing at 6.8% in January 2026.

Total retail sales also followed a positive trajectory, albeit with less volatility and generally lower growth rates than TCF. Following modest growth in the early part of the year, retail sales strengthened during the summer and autumn, reaching 4.8% in September and peaking at 4.9% in October. Growth remained solid through the end of the year, accelerating further to reach 6.5% in January 2026, which suggests a broad-based improvement in retail activity.

On the consumer side, footwear expenditure remained broadly flat throughout the year. Average monthly spending stood at 982 pounds in the first quarter of 2025 and edged slightly down to 981 pounds in the second quarter, before stabilising and increasing to 988 pounds during the summer months.

Despite these positive developments, consumer behaviour remains cautious. Surveys suggest that overall spending growth has been subdued, with households becoming more selective in their purchases and more likely to delay or reduce discretionary spending amid ongoing economic uncertainty and inflation concerns (reuters.com).

Although retail sales values increased throughout the year, the average consumer expenditure on footwear remained broadly stable. This divergence reflects the fact that growth in retail turnover has not been driven by higher spending per consumer, but rather by an increase in the number of transactions and/or the number of active consumers. In other words, aggregate sales are rising even though individual spending remains constrained.

This pattern is consistent with a more cautious consumer environment, in which households continue to participate in the market but make smaller, more frequent purchases rather than larger discretionary outlays.

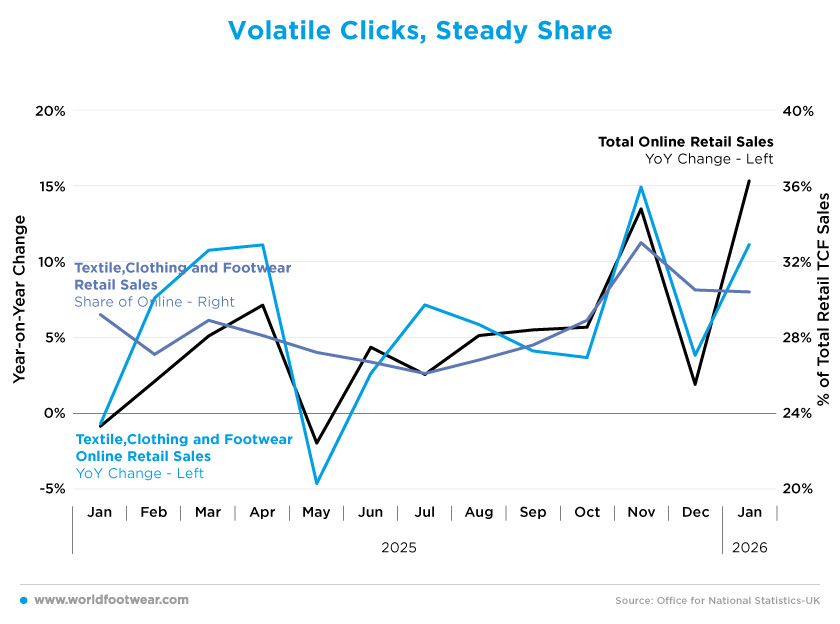

Volatile Clicks, Steady Share

Online retail sales in the UK followed a broadly positive but volatile trajectory throughout 2025.Following a 0.9% contraction in January, online sales recovered strongly in the subsequent months, reaching growth rates above 7% in April. However, volatility persisted, with a further contraction in May (-2.0%) before growth resumed and accelerated significantly towards the end of the year. November and January 2026 stood out, with particularly strong increases of 13.5% and 15.3%, respectively.

Recent data shows that online retail performance in the UK has been uneven, with non-food online sales declining in some months and overall growth lagging behind historical averages. At the same time, adverse weather conditions and declining footfall in physical stores have contributed to a shift towards online shopping, with consumers increasingly favouring the convenience it offers (brc.org.uk).

A similar but more pronounced pattern was observed in online sales of textile, clothing and footwear (TCF). After a slight decline in January, TCF online sales surged in the spring months, reaching double-digit growth in March and April. This was followed by a sharp drop in May (-4.6%), but sales recovered again during the summer. Growth remained positive but more moderate through early autumn before accelerating again towards the end of the year, peaking at 14.9% in November and remaining strong at 11.1% in January 2026.

Despite this volatility, the share of online sales within total TCF retail remained relatively stable throughout the year. It fluctuated between approximately 26% and 30%, with a noticeable increase toward the end of the year to exceed 30% in November, remaining at this level into early 2026. This suggests a gradual strengthening of online channels within the fashion sector.

More broadly, consumer behaviour continues to reflect a cautious environment, with spending patterns remaining selective and influenced by ongoing economic uncertainty, including concerns about inflation and household finances (reuters.com).

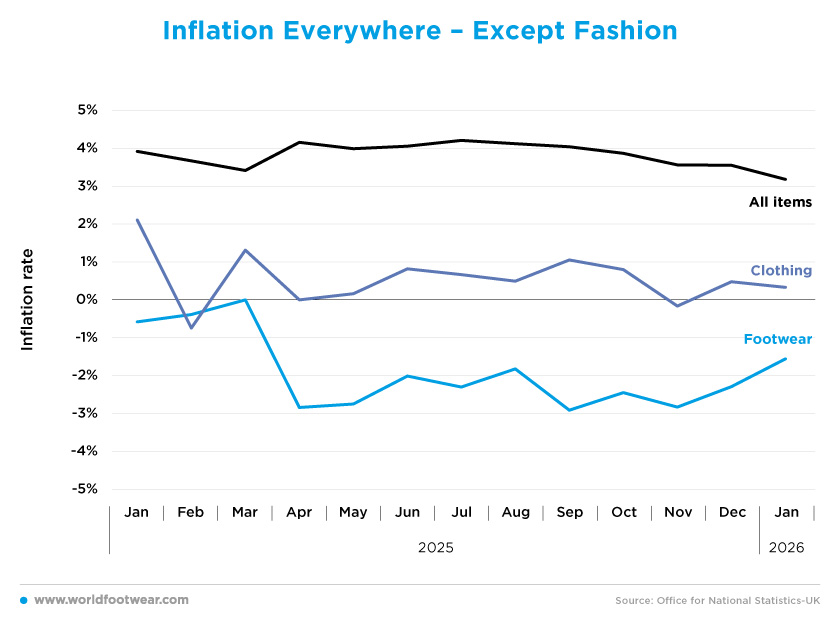

Inflation Everywhere – Except Fashion

In 2025, price dynamics in the UK retail sector showed a clear divergence between overall inflation and fashion-related categories. Although headline inflation remained high, fluctuating between 3.4% and 4.2% for much of the year, it gradually eased towards the end of the period, reaching 3.2% in January 2026.At the same time, intense competition within the retail sector, particularly in non-food categories such as fashion, is reflected in price dynamics. Despite broader inflationary pressures, retailers have continued to rely on promotions and competitive pricing strategies, helping to keep price increases subdued (brc.org.uk).

Regarding the footwear sector, prices remained consistently negative throughout the year. Starting at -0.6% in January, footwear inflation declined further, reaching lows of around -2.8% to -2.9% in several months, including April, September and November. Even by January 2026, footwear prices were still contracting by 1.6% year-on-year, indicating persistent discounting across the sector.

Clothing prices followed a more stable pattern but remained subdued. After growing slightly in the early part of the year, clothing inflation hovered close to zero for much of the period, briefly turning negative in November. Overall, price increases in clothing remained modest compared to the broader inflation environment.

The persistent gap between rising sales and falling or stagnant prices suggests that volume growth in the fashion sector is being driven largely by discounting and promotional activity, rather than by an improvement in consumers’ real purchasing power.

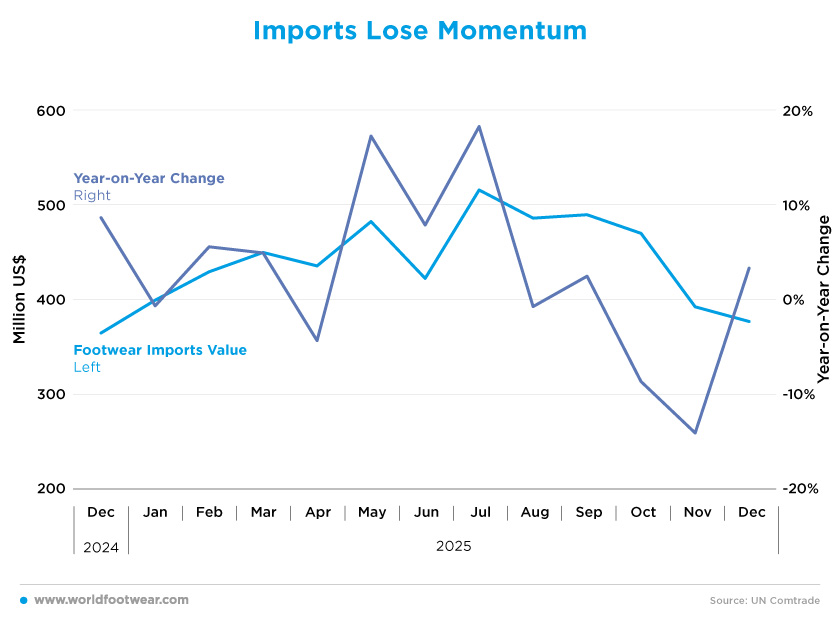

Imports Lose Momentum

Footwear imports into the UK showed significant volatility throughout 2025, closely reflecting fluctuations in retail performance.Following a modest year-on-year decline of 0.7% in January 2025, imports recovered in subsequent months, with steady growth in February and March. However, this momentum was interrupted in April, when imports fell by 4.3%. They then rebounded strongly in May with a 17.3% increase.

The most notable shift occurred in the middle of the year. After strong growth in May, imports slowed in June, rising by 7.9% year-on-year but remaining below the peak levels seen in previous months. This was followed by a sharp acceleration in July, when imports surged by 18.3% to reach the highest monthly value of the year. This rebound suggests a rapid adjustment in ordering patterns in response to earlier fluctuations in retail demand.

In the second half of the year, import growth became more uneven. While September saw a modest increase of 2.5%, imports declined again in October, dropping sharply by 14.1% in November, before recovering slightly in December with a 3.3% increase. This pattern suggests a high degree of responsiveness among importers to changing market conditions.

The sharp fluctuations in import volumes throughout the year suggest that retailers are becoming more reactive in their inventory management, with retailers adjusting orders quickly in response to short-term changes in sales performance and demand expectations.

According to the British Retail Consortium, retailers are still operating in a challenging environment, facing rising costs, uncertainty around taxation and persistent pressure on consumer spending. Industry leaders have warned that concerns about inflation, business rates and household finances are influencing both investment decisions and inventory strategies, particularly during key trading periods.