Register to continue reading for free

US Retail: footwear under pressure as retail holds

Although overall sales remained stable in 2025, performance within the fashion sector was mixed, with clothing outperforming the far more volatile footwear segment. At the same time, weakening consumer sentiment persisted despite easing monetary policy, signalling growing uncertainty. This is particularly evident in footwear imports, which reversed sharply after a strong start to the year and declined alongside retail sales, even as import prices continued to rise. The combination of falling volumes and higher costs points to a sector increasingly squeezed by soft demand and ongoing supply-side issues

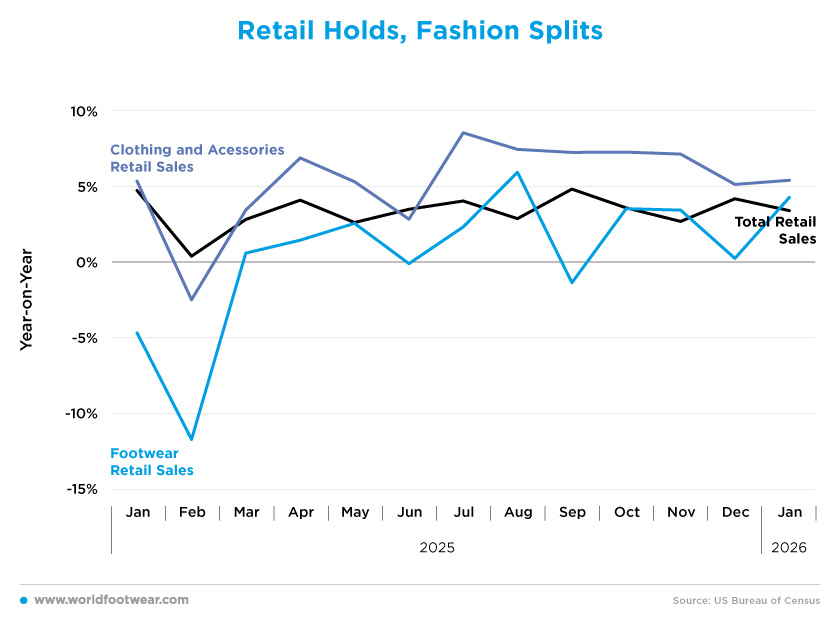

Retail Holds, Fashion Splits

Retail sales in the United States (US) remained resilient throughout 2025, with total retail sales consistently posting positive year-on-year growth. After a strong start to the year at 4.7% in January, growth slowed sharply in February to 0.4%, before recovering in the following months. From March onwards, retail sales remained within a relatively stable range of around 2.6% to 4.8%, ending the year at 4.2% in December and continuing at 3.4% in January 2026.According to the National Retail Federation, this steady performance is indicative of a broader pattern of resilience in US consumer spending, which has supported retail activity despite economic uncertainty. Retail data shows that spending has remained strong on a year-on-year basis, with multiple categories posting solid gains and consumers continuing to drive growth.

Clothing and accessories sales outperformed the broader retail sector for most of the year. Following a brief contraction in February (-2.4%), the segment experienced a strong rebound, achieving a 6.9% growth in April and remaining consistently elevated thereafter. From July to November, clothing sales growth stayed above 7%, peaking at 8.5% in July, and maintained a strong momentum through the second half of the year, before moderating slightly to 5.1% in December, and returning to 5.4% in January 2026.

By contrast, footwear sales displayed significant volatility. The year began with sharp contractions, with sales falling by 4.6% in January and 11.6% in February, before recovering to positive territory in March. Growth remained uneven throughout the year, fluctuating between gains and losses, including a further contraction in September (-1.3%). However, the segment strengthened towards the end of the year, with growth reaching 3.5% in both October and November, and reaching 4.3% in January 2026.

This divergence suggests that while overall retail demand has remained stable, consumer spending within the fashion sector has been uneven. Clothing has benefited from stronger and more consistent demand, whereas footwear appears to have been more sensitive to short-term shifts in purchasing behaviour.

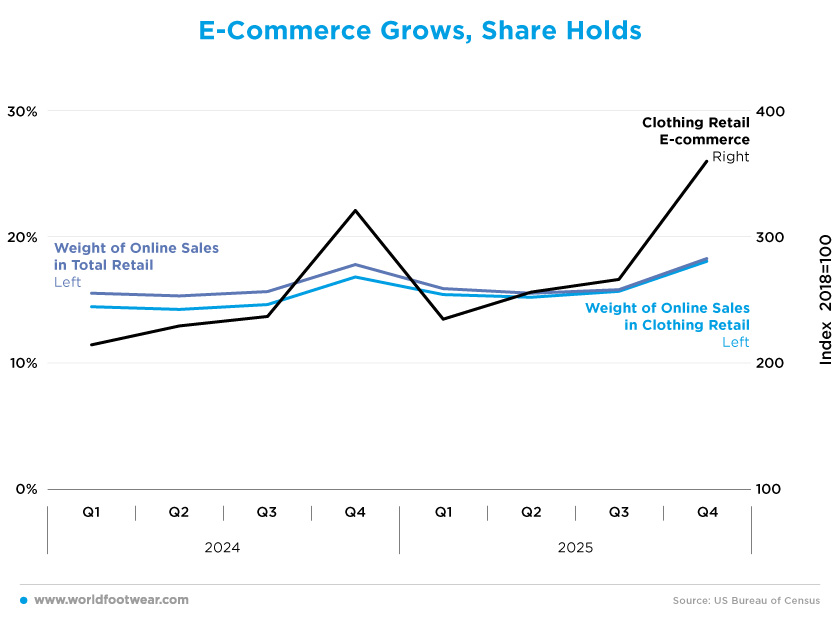

E-Commerce Grows, Share Holds

Throughout 2025, e-commerce continued to play a stable but expanding role in US retail, with growth driven more by seasonal dynamics than by structural shifts in consumer behaviour. The proportion of sales made online remained relatively consistent during most of the year, fluctuating between 15.5% and 15.9% across the first three quarters, before rising more sharply to 18.3% in the final quarter.A similar pattern can be observed in the clothing segment. During the first three quarters of the year, the weight of online sales in clothing retail hovered around 15–16%, showing only marginal increases compared to 2024. However, the share rose significantly to 18.0% in the fourth quarter, highlighting the importance of the holiday season in driving online activity.

In contrast, the value of clothing e-commerce sales showed a more pronounced upward trend. Following a dip in early 2025 compared to the strong end of 2024, the index recovered steadily throughout the year. It rose from 235 in the first quarter to 266 in the third quarter, before surging to 360 in the fourth quarter. This represents a substantial increase not only year-on-year but also compared to pre-holiday levels.

The combination of stable online penetration and rising e-commerce values suggests that digital channels are growing in line with the broader market, rather than gaining a significant additional share. This points to a more mature phase of e-commerce adoption in the US.

According to a recent report from Forrester, online sales could reach 1.8 trillion US dollars by 2030, accounting for nearly 30% of total retail. However, at the same time, some indicators suggest that the market is maturing, with the proportion of consumers shopping online daily declining in recent surveys. This could mean that future growth will come more from value expansion than from increased penetration (retaildive.com).

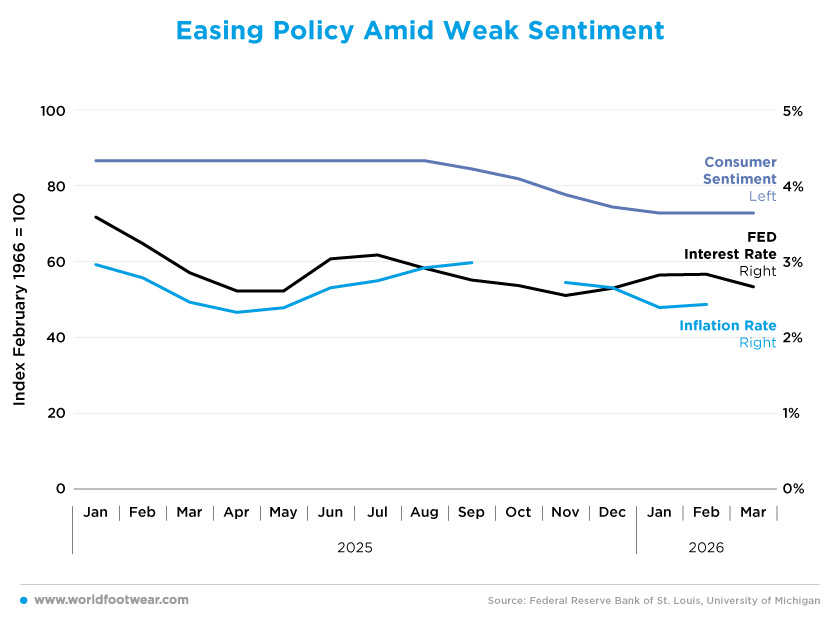

Easing Policy Amid Weak Sentiment

Inflation in the US showed a relatively contained but fluctuating pattern throughout 2025. After opening the year at 3.0% in January, it declined steadily to a low of 2.3% in April, before gradually rising again to reach 3.0% in both September and October. Towards the end of the year, inflation eased once more, settling at 2.7% in November and December, before falling further to 2.4% in the first months of 2026.Interest rates followed a different trajectory. The Federal Reserve maintained its benchmark rate at 4.3% for most of the year, from January through August, before beginning a gradual cycle of interest rate cuts. Rates were reduced to 4.2% in September and continued to decline through the final quarter, reaching 3.7% by December and stabilising at 3.6% in early 2026.

This policy shift reflects mounting concerns about the wider economic outlook, particularly in the labour market, where signs of deteriorating conditions have prompted a more accommodating stance. Meanwhile, inflationary pressures – partly linked to external shocks, such as rising energy prices – have persisted, making it difficult for the Federal Reserve to balance price stability with economic support.

Consumer sentiment deteriorated markedly over the course of the year. Starting from a relatively solid level of 71.7 in January, the index declined sharply to 52.2 by April and remained subdued throughout the rest of the year, reaching a low of 51.0 in November. Although there was a modest recovery in sentiment at the start of 2026, with an increase to 56.6 in February, this remained well below the levels observed at the beginning last year.

Some surveys indicate that consumers are increasingly concerned about inflation, job prospects and the broader economic environment, with rising energy prices and financial market volatility having a negative impact on expectations. While higher-income households have continued to support spending, the overall sentiment remains fragile, highlighting the risk of weaker consumption ahead (reuters.com).

The combination of easing inflation, falling interest rates and weak consumer sentiment suggests that the US economy is entering a more uncertain phase. Although monetary policy is becoming more supportive, confidence has yet to recover. This helps to explain why, while retail activity has remained resilient overall, it has been uneven across sectors.

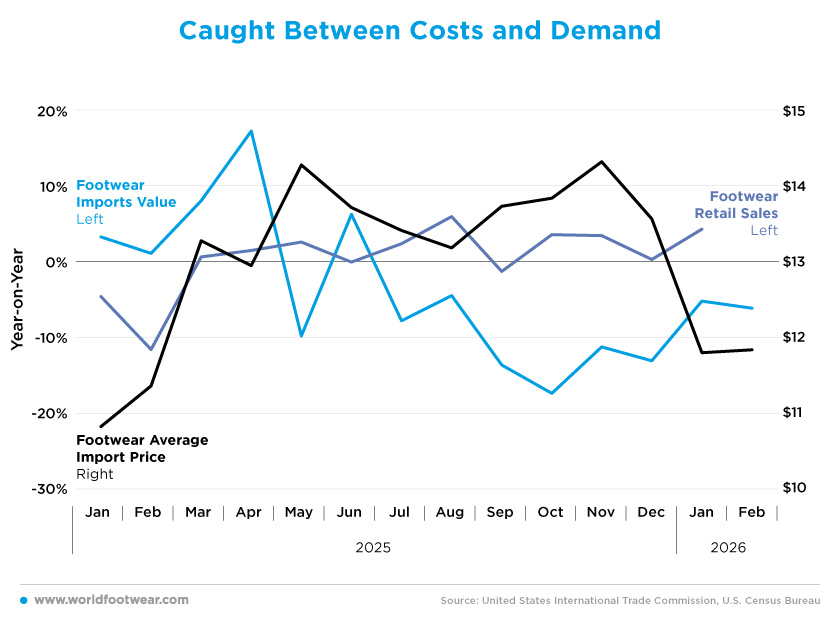

Caught Between Costs and Demand

Footwear imports to the US showed a clear shift in momentum over the course of 2025. After a relatively strong start to the year, with import values increasing by 3.3% in January and accelerating to 17.2% in April, the trend suddenly reversed in subsequent months. From May onwards, imports remained consistently negative, with the decline deepening to -17.4% in October and staying below -10% through the end of the year. This contraction continued into early 2026, with imports still down 6.1% in February.The same pattern was seen in retail sales in footwear stores. Following a strong performance in April (+13.3%), sales declined sharply in the succeeding months, turning negative in May (-19.6%) and remaining weak for the rest of the year. The contraction deepened in the autumn, with sales falling by as much as 19.5% in October, remaining negative into early 2026.

By contrast, the average import price of footwear increased throughout most of the year. Starting at 10.82 US in January, prices rose steadily, peaking above 14 US dollars in several months, including May and November. Although there was some moderation at the start of 2026, prices remained higher than in early 2025 levels, suggesting ongoing cost pressures in the supply chain.

This increase in import costs reflects the broader structural pressures currently affecting the footwear industry, particularly in terms of trade policy uncertainty and tariff-related disruptions. Recent developments in US trade policy, including the introduction and subsequent adjustment of tariffs on key trading partners, have forced companies to reconsider their sourcing strategies and adapt their supply chains to mitigate rising costs (wwd.com).

The simultaneous increase in import prices and decline in retail sales suggests that rising costs are being shared across the market. On the one hand, higher prices indicate that consumers are absorbing part of the tariff-related cost increases. On the other, the sharp contraction in sales points to weakening demand, implying that firms are also bearing part of the burden through lower sales volumes.

This dynamic highlights a broad-based squeeze, where both consumers and retailers are affected by rising costs and constrained demand.