Register to continue reading for free

Global footwear trade weakens in early 2026

International footwear trade began 2026 under pressure. In the first quarter of the year, most of the main production-based exporters analysed recorded a decline in exports, while several major consumption markets also reduced their imports. The results point to a cautious start to the year for global footwear, although the impact varied substantially across country profiles

To avoid confusing production gains with distribution activity, the analysis distinguishes between three country profiles*: producer-exporters, re-export hubs and consumption importers. This distinction is particularly relevant in footwear trade, where some countries play a major role as logistics or re-export platforms despite having limited domestic production.

As the focus of the article is global trade, the analysis includes ten export-oriented countries reflecting actual production (represented in the producer-exporters group) and ten import-oriented countries that do not have relevant production (divided into re-export hubs and consumption importers groups).

Producer-exporters lose momentum

Among the ten producer-exporters analysed, footwear exports fell by 12.3% in value (from 22.2 to 19.5 billion euros) in the first quarter of 2026, compared with the same period of the previous year. The decline was broad-based, with all countries in this group recording negative year-on-year growth.Where data in pairs are available, the decline in volume was more moderate. Taken together, China, India, Italy, Spain, Portugal and Brazil exported 2.31 billion pairs of footwear in the first quarter of 2026, 3.2% less than in the same period of 2025. This suggests that part of the decline in export value may also reflect price and product-mix effects, not necessarily a reduction in the number of pairs exported.

China remained by far the largest exporter in the group, but its footwear exports fell by 17.6% in the first quarter. After exporting 9.75 billion euros in the first three months of 2025, China exported 8.03 billion euros in the same period of 2026. The decline was particularly sharp in March, when exports fell to 1.66 billion euros, compared with 2.94 billion euros one year earlier. In volume, however, the decline was much more contained, with exports decreasing by 2.5%, from 2.15 billion pairs to 2.10 billion pairs.

Vietnam’s footwear exports declined by 9.3%, from 5.11 billion euros in the first quarter of 2025 to 4.63 billion euros in the first quarter of 2026. Indonesia followed the same trend, with exports decreasing by 10.9%, from 1.74 billion euros to 1.55 billion euros.

India’s exports fell by 19.5% in value, while Türkiye and Brazil recorded the steepest contractions among the countries analysed: Turkish footwear exports declined by 27.9% (from 302 million euros to 218 million euros), while Brazil’s exports fell by 29.6% (from 256 million euros to 180 million euros). By contrast, Mexico posted a relatively moderate decrease, with exports down by 4.4%.

European producer-exporters showed more resilience in value, although they also remained in negative territory. Italy’s footwear exports decreased by only 1.6%, from 3.04 billion euros to 2.99 billion euros. However, in volume, Italian exports fell by 15.2%, from 60.5 million pairs to 51.3 million pairs, suggesting an increase in the average export price or a shift towards higher-value products.

Spain’s exports fell by 3.8% in value (from 977 to 940 million euro), but increased by 0.5% in volume, reaching 46.3 million pairs in the first quarter of 2026. Portugal recorded a decline both in value (4.3%) and in volume (7.1%), exporting 432 million euros and 19.3 million pairs in the same period.

The results suggest that, at least in value terms, the first quarter of 2026 was marked by a general slowdown among the main production-based footwear exporters. However, the scale and nature of the decline varied significantly.

While China recorded a sharp fall in value but only a slight decrease in pairs, Italy showed the opposite pattern, with a mild value decline but a stronger reduction in volume. Spain, meanwhile, increased exports in pairs despite a fall in value, whereas Portugal decreased both in value and volume.

Re-export hubs show a divided picture

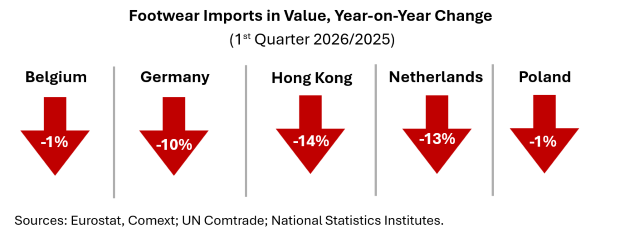

Regarding imports, starting with the group of five re-export hubs, the first quarter of 2026 recorded a 7.9% decline in value of footwear imports (from 8.6 to 7.9 billion euros). In volume, the decline was also visible, although less pronounced: imports fell by 5.5%, from 506.5 million pairs to 478.8 million pairs. However, the aggregate result hides different national performances.Belgium remained close to stability in value, with imports decreasing by only 0.6%. After importing 1.32 billion euros in footwear in the first quarter of 2025, Belgium imported 1.31 billion euros in the same period of 2026. In volume, Belgian imports increased by 4.2%, from 67.2 million pairs to 70.0 million pairs.

Hong Kong recorded a decline, both in value and volume. Footwear imports fell by 13.6% in value (from 425 million euros to 367 million euros), and by 4.8% in volume (from 18.7 million pairs to 17.8 million pairs). Germany also recorded a pronounced decline, with imports decreasing by 9.5% in value (from 3.72 billion euros to 3.37 billion euros) and by 6.1% in volume (from 214.7 million pairs to 201.6 million pairs).

The Netherlands and Poland also remained in negative territory. Dutch footwear imports decreased by 13.3% in value (from 1.83 billion euros in the first quarter of 2025 to 1.59 billion euros in the same period of 2026) and by 8.0% in volume. Poland recorded a comparatively moderate fall in value, with imports down by 1.3%, but a stronger decline in volume, at 8.3%.

These figures show why re-export hubs need to be analysed separately from consumption importers. Changes in countries such as the Netherlands, Poland, Germany or Belgium may reflect distribution activity, intra-European trade flows, logistics patterns or stock-management decisions, and should not be interpreted automatically as signs of stronger or weaker domestic footwear demand.

Consumption importers point to softer demand

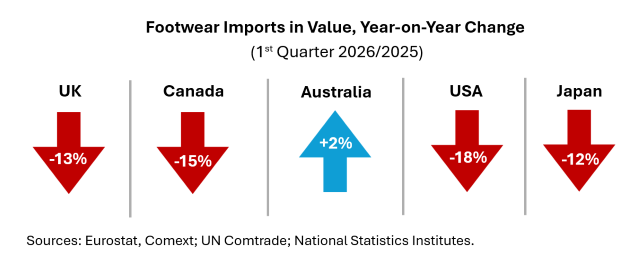

Among the five main consumption importers analysed, footwear imports fell by 15.6% in value (from 10.4 to 8.8 billion euros) in the first quarter of 2026. In volume, the decline was also significant, with imports falling by 9.1%, from 935.6 million pairs to 850.3 million pairs. This group includes the United States, Japan, the United Kingdom, Canada and Australia — markets where imports are more closely associated with domestic consumption than with re-export activity.The United States, the largest consumption importer in the sample, recorded an 18.0% decline in value: imports fell from 6.75 billion euros in the first quarter of 2025 to 5.53 billion euros in the same period of 2026. In volume, imports decreased by 11.8%, from 601.1 million pairs to 530.1 million pairs. The decline was visible across all three months, confirming a weaker start to the year in the world’s largest footwear import market.

Japan also recorded a negative performance, although the decline was sharper in value than in volume. Imports fell by 12.1% in value, from 1.36 billion euros to 1.19 billion euros, while volume decreased by only 1.7%, from 167.7 million pairs to 164.8 million pairs. This suggests a lower average import price in the first quarter of 2026.

The United Kingdom’s imports declined by 13.1% in value and by 8.1% in volume, while Canada recorded falls of 14.9% and 12.6%, respectively. Australia was the only consumption importer in the group to post growth: its imports increased by 2.2% in value and by 5.0% in volume, reaching 33.7 million pairs in the first quarter of 2026.

The overall picture among consumption importers points to weaker demand in several mature markets at the beginning of 2026. The decline in the United States is particularly relevant, given the size of the market and its importance for global footwear exporters.

A weaker start, but not a uniform one

Taken together, the data suggest that global footwear trade began 2026 with clear signs of weakness, pointing to a softer international environment for footwear trade in the first quarter of the year. However, the picture is not uniform.European producer-exporters such as Italy, Spain and Portugal recorded more moderate declines than several Asian and Latin American exporters, although volume dynamics differed considerably between them. At the same time, some re-export hubs analysed also moved into negative territory in value, although the scale of the decline differed significantly between countries: Belgium and Poland remained close to stability, while Germany, the Netherlands and Hong Kong recorded more pronounced falls.

The distinction between producer-exporters, re-export hubs and consumption importers is therefore essential. Without it, import growth in distribution hubs could be misread as stronger final consumption. By separating these profiles, the data show a more nuanced picture: global footwear trade weakened in early 2026, but the adjustment varied according to each country’s role in the international value chain.

*Countries were grouped according to their role in global footwear trade:

- The group of producer-exporters includes countries that are both among the world’s top 25 footwear producers and among the top 10 footwear exporters. This criterion was used to identify economies whose export performance is more closely linked to domestic production capacity.

- The group of re-export hubs includes countries among the bottom 60 footwear producers that nevertheless record above-average import values, but the key criterion is that exports must represent at least 50% of their imports. This profile identifies countries where trade flows are likely to reflect re-export activity rather than domestic production.

- The group of consumption importers includes countries that also have limited production and significant imports, but whose exports represent less than 20% of their imports. This profile identifies markets where imports are more closely associated with domestic consumption than with onward distribution.

Where recent trade data were not available for countries meeting these criteria, the analysis moved to the next country in the ranking for which data were available.

Image Credits: Ayrus Hill on Unsplash