Register to continue reading for free

Japan Retail: too early to be excited about retail

After a year of underperforming, the Retail Index for Apparel & Accessories managed to overcome the figures of the previous year in March 2021. Notwithstanding, importers do not seem yet convinced that this is a sustained recovery. The good news, as in other countries, comes from confidence indicators, with consumers seem to drive away from pessimism. However, all seems too fragile yet and it might mean that it is too early to get excited with retail in Japan

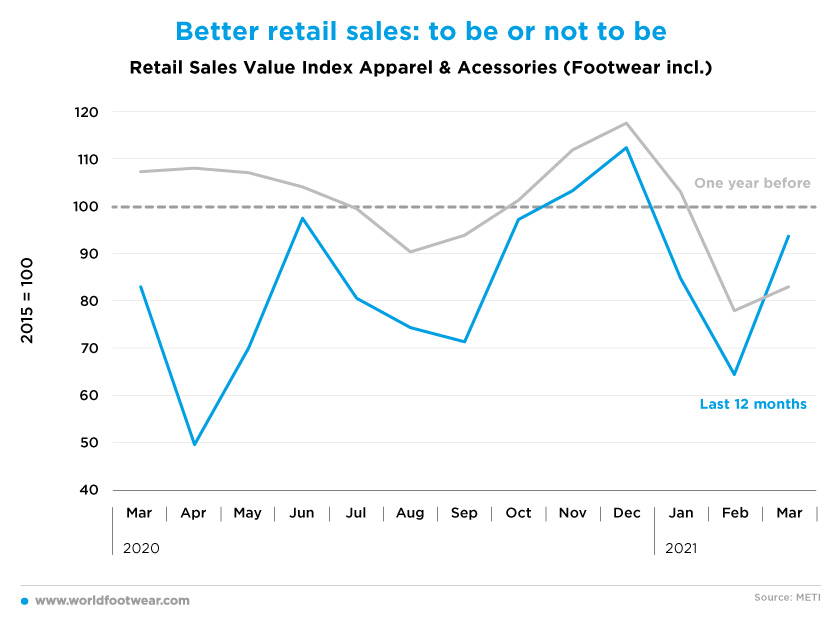

Better retail sales: to be or not to be

According to the Retail Index for Apparel & Accessories (including footwear) sales have been recovering in line with the previous year seasonal pattern since last October through December. The slight and stable gap - 4 to 8 percentage points (pp) - compared to 2019 translates the low COVID-19 scores for the period.

Despite the COVID-19 indicators, which at the beginning of 2021 were the worst of the pandemic so far, the retail gap increased by only 10 more pp. Such a small widening of the gap stems from the fact that the two first COVID–induced retail depressions (April and August 2020) are compared to 2019 pre-COVID times; in the months of January-February COVID-19 was present both in 2020 and 2021.

Apparently, the good news came in March 2021 with COVID-19 fading away and retail overcoming the previous year performance for the first time, and despite the pandemic incidence in March this year being stronger than a year before.

This might indicate a new breath of fresh air for businesses after months of feeling the hit of the pandemic in their sales. Japanese retail giant Aeon Co., for example, has reported a group net loss of 71 million Japanese ienes (0.54 million euros) for the year through February, the first red ink in 12 years.

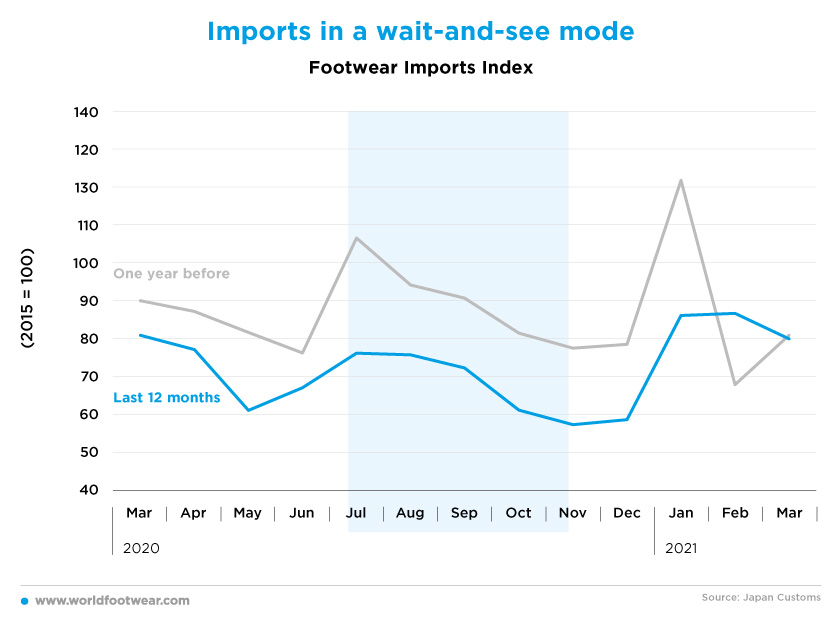

Footwear Imports

The increase of footwear imports is seasonally usual in January, advancing the next retail season. Nevertheless, the strong COVID-19 peak effect in January 2021 is clearly present: compared to the previous year the monthly imports loss increased from 19 points in December 2020 to 36 pp in January 2021. After that, footwear imports moved from stabilization in February to further weakening in March, closing at a similar level as the one registered in the same month in 2020. This inconstant behaviour seems to indicate that importers are not yet convinced about a sustained retail recovery.

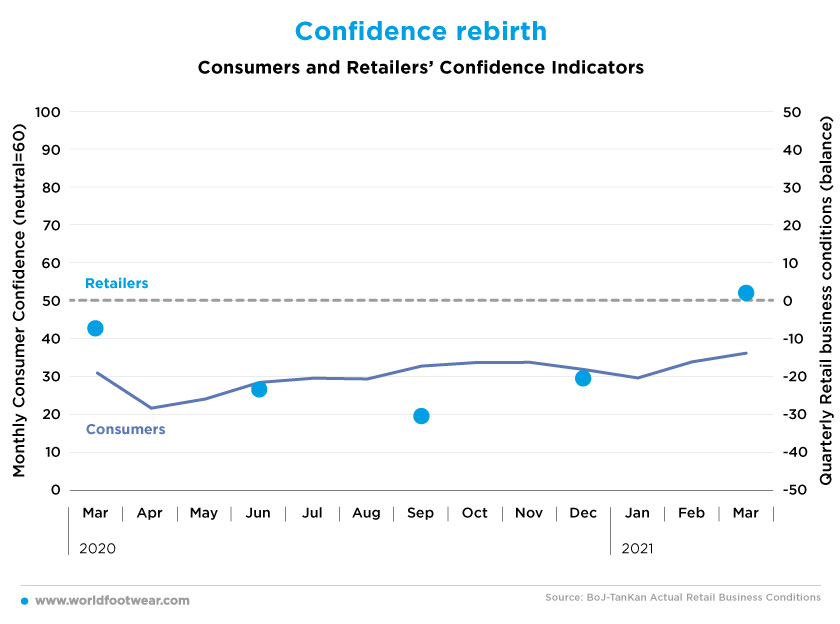

Confidence rebirth

On the contrary, confidence indicators are giving some support to good retail expectations. Consumers are gradually driving away pessimism, for two successive months, while retailers’ actual view of business conditions in March is on the upside, against a negative picture all along 2020.In fact, the Japan Department Stores Association reported department store sales jumped 21.8% in March, with sharp gains in clothing (+24%) and accessories, following the lifting of the second state of emergency, declared in January 2021.This was the first year-on-year gain in 18 months and compares with a 33.4% plunge one year ago.

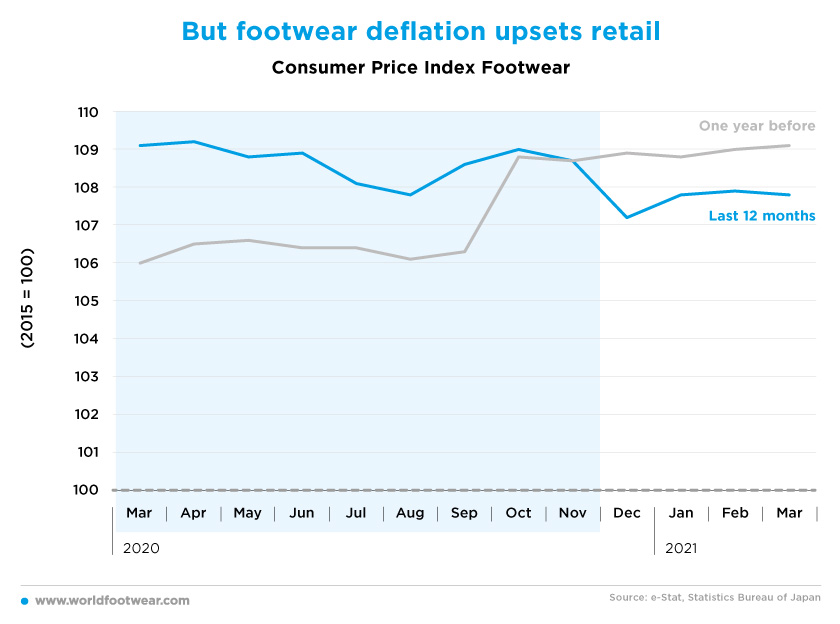

But footwear deflation upsets retail

In the last four months ending in March the evolution path of the Consumer Price Index for footwear is disappointing. Compared with the same period in 2020 footwear price deflation is far from good for retailers.

All taken together this might indicate that it is too early to be excited about retail. The vaccine rollout is trailing behind other advanced countries while a fourth wave of the pandemic is back in April with a third state of emergency scheduled to last through May and affecting all the biggest Japanese metropolitan areas, supposed to close all sections other than food or cosmetics of large shopping facilities such as department stores. This impacted the Golden Week holiday season, as many retailers and department stores complained. In fact, a survey by travel agency JTB Corp has shown that consumers were not in a travel mood and just 10% said they would travel during the holidays (in previous years, that percentage reached 25%).

Should these signs prevail, better short-term business forecasts will be frustrated. Looking ahead, the Olympic Games in July could be the next opportunity to boost retail.

And perhaps, recovery is still farther away. After posting the first annual net loss in 17 years the major Japanese department store chain Takashimaya said it is uncertain when demand from domestic shoppers and inbound tourists will recover, expecting things to return to the pre-pandemic level not before the 2022-23 business year.