Register to continue reading for free

Netherlands Retail: Confidence gap widens, footwear lags

Recent developments in the Dutch retail market reveal an increasing gap. Although consumer confidence has deteriorated sharply, retailers remain positive and footwear imports have shown resilience. Yet, footwear continues to lag behind the broader retail sector, facing weaker demand, persistent price pressure, and inconsistent sales. Meanwhile, online retail remains structurally strong, reflecting the ongoing shift in consumer purchasing behaviour

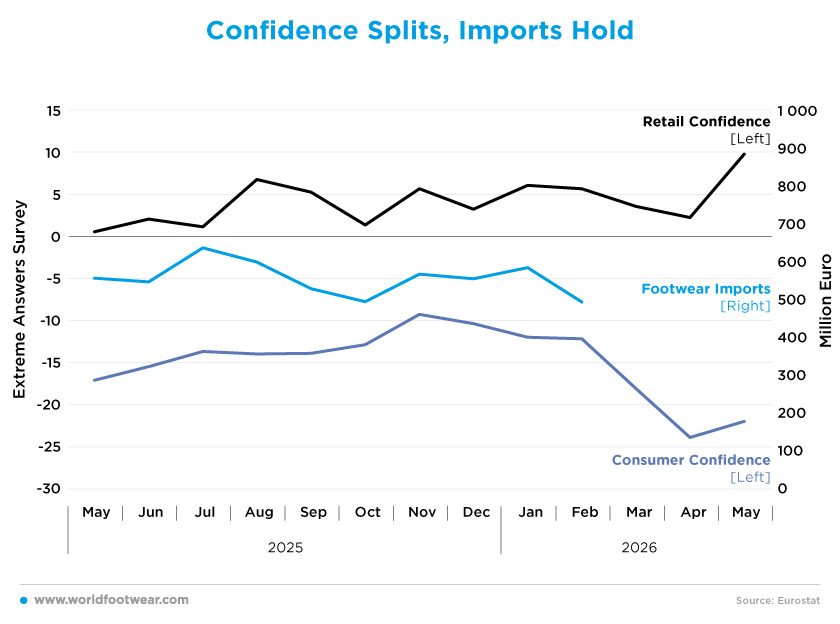

Confidence Splits, Imports Hold

Consumer and retail sentiment in the Netherlands moved in sharply different directions during the period analysed. Consumer confidence remained negative throughout, improving from -17.1 in May 2025 to -9.3 in November, before weakening again at the start of 2026. From March onwards, the deterioration became much more pronounced, with the indicator falling to -18.1 in March, -23.9 in April and -22.0 in May.Retail confidence, by contrast, remained positive throughout the entire period. After starting at 0.5 in May 2025, it rose to 6.7 in August and remained above zero in every month thereafter. Even when consumer confidence deteriorated sharply in spring 2026, retail confidence remained positive. It fell to 2.2 in April, but then rebounded strongly to reach 9.7 in May.

This divergence comes against a backdrop of weakening household sentiment. Recent figures point to a sharp deterioration in consumer confidence in March, April and May, driven by more negative views of the economy and a weaker willingness to buy. The fall in April was described as the second-largest monthly decline since the series began, surpassed only by the drop recorded at the start of the pandemic (cbs.nl).

Although Dutch households continue to benefit from relatively strong wage growth, pension increases and low unemployment, higher energy prices and renewed geopolitical uncertainty are likely to encourage a more cautious approach to spending. In practice, this means that a larger share of income gains may be saved rather than spent, thereby limiting growth in consumer spending (think.ing.com).

Although footwear imports fluctuated, they did not show a clear downward trend in the months for which data is available. Imports stood at 556 million euros in May 2025, peaked at 636 in July, fell to 494 in October, and then recovered to 583 in January 2026 before dropping again to 493 in February. As import data is only available up to February, it is not yet possible to assess whether the sharp fall in consumer confidence from March onwards affected footwear import behaviour.

The main message is therefore not simply a collapse in retail conditions, but a growing disconnect: consumers have become much more pessimistic, while retailers remain comparatively confident, and import flows have remained relatively resilient so far.

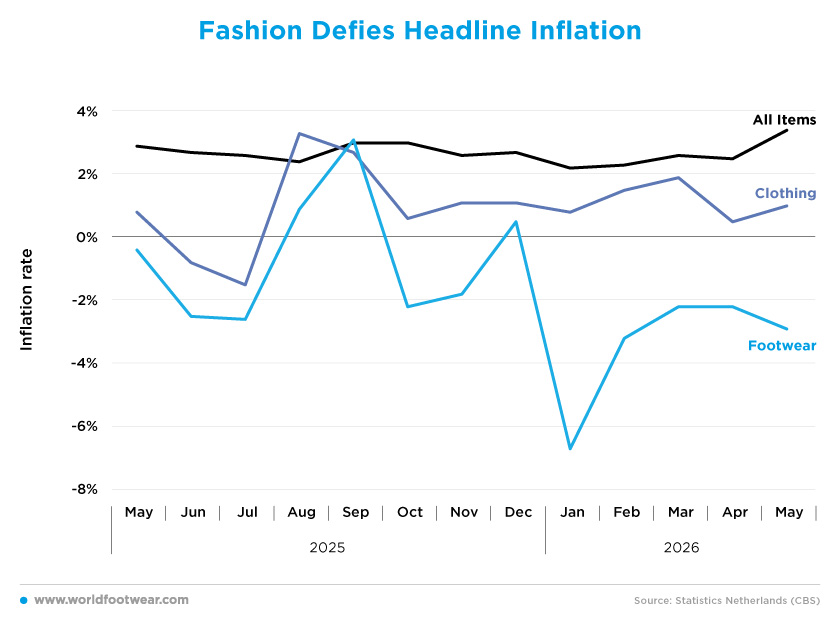

Fashion Defies Headline Inflation

General inflation in the Netherlands remained relatively consistent over the analysed period, fluctuating within a relatively narrow range for most of the year while staying positive. However, price developments in clothing and footwear followed a very different path, with footwear prices in particular falling throughout most of the period.In May, all-items inflation stood at 2.9%, easing to 2.4% in August, and then returning to around 3.0% in September and October. After falling to 2.2% in January 2026, inflation gradually increased again, reaching 3.4% in May 2026. This latest rise in headline inflation reflects a broader environment in which consumer prices remain under pressure.

Recent figures show that consumer goods and services became more expensive in May, while higher energy and fuel prices are expected to keep inflation above previous expectations, feeding gradually into other goods and services (cbs.nl). The persistence of price pressures is also reflected in the wider euro area policy environment, with the European Central Bank raising its key interest rates by 25 basis points in June.

Clothing inflation was more uneven. Prices fell in June and July 2025, before rising sharply in August and September to reach 3.3% and 2.7%, respectively. From October onwards, clothing inflation moderated and remained relatively low, fluctuating between 0.5% and 1.9% through May 2026.

Footwear prices followed an even weaker path. Inflation was negative in most months, falling by 2.5% in June and 2.6% in July 2025. It turned positive briefly in August and September, before falling again in October and November, and then turning positive again in December. Prices declined sharply in early 2026, with the steepest fall occurring in January, when prices were 6.7% lower year-on-year. By May 2026, footwear inflation remained negative, at 2.9%.

The contrast between persistent headline inflation and negative footwear inflation suggests that footwear retailers may be under pressure to offer discounts or absorb costs, rather than passing on the full impact of broader inflationary pressures to consumers.

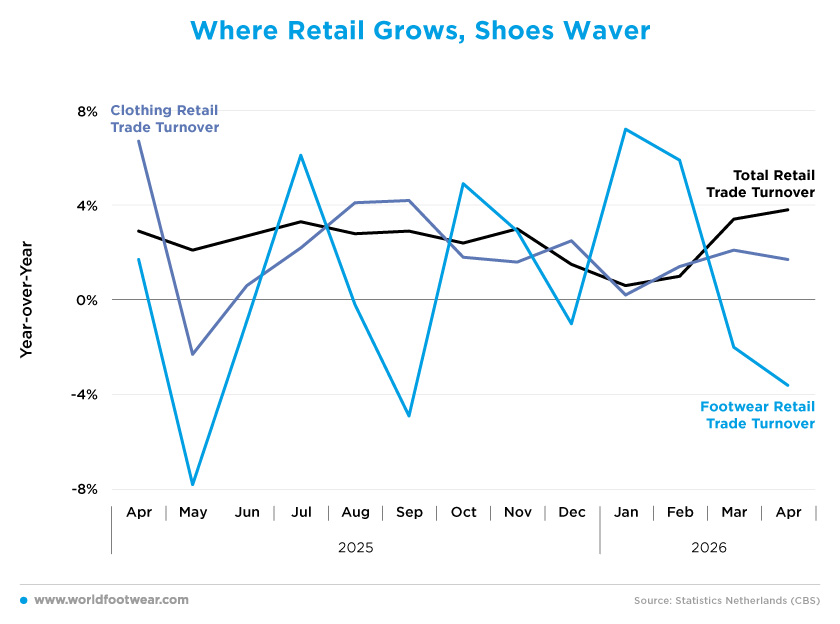

Where Retail Grows, Shoes Waver

Retail turnover in the Netherlands remained positive throughout the period analysed, but the footwear sector was more volatile than both the wider retail market and clothing. While total retail trade turnover showed steady growth, footwear alternated between strong gains and sharp contractions.Growth in total retail was relatively stable for most of 2025, fluctuating between 2.1% and 3.3%, before slowing at the start of 2026. However, it still increased in every month and recovered slightly towards the end of the first quarter, ranging from 0.6% in January to 3.8% in April.

Although clothing retail turnover was less consistent than total retail, it also remained mostly positive. It grew strongly in April 2025, at 6.7%, before falling by 2.3% in May. From June onwards, clothing turnover returned to positive territory and remained there through April 2026. However, growth generally moderated, staying between 0.2% and 4.2%.

Footwear retail turnover was much more volatile. After a modest increase of 1.7% in April 2025, turnover fell sharply in May (-7.8%) and remained negative in June. It then rebounded strongly in July, growing by 6.1%, before fluctuating between contractions and recoveries in the subsequent months. The strongest performance occurred at the start of 2026, with footwear turnover rising by 7.2% in January and 5.9% in February. However, this momentum was short-lived, with turnover falling again in March (-2.0%) and April (-3.6%).

The weakness in the footwear sector is particularly notable because it contrasts with the broader retail picture. This same contrast is visible in household consumption. In April, consumers spent more on durable goods, particularly passenger cars, home furnishing and electrical appliances, while total household consumption also increased in volume terms. This suggests that Dutch consumers were still spending in some discretionary categories, even as footwear sales remained weak (cbs.nl).

Therefore, the key point is not just that footwear turnover was volatile, but also that footwear failed to benefit from the resilience seen in the wider Dutch retail sector and some other consumer categories. This suggests that the underperformance is more sector specific.

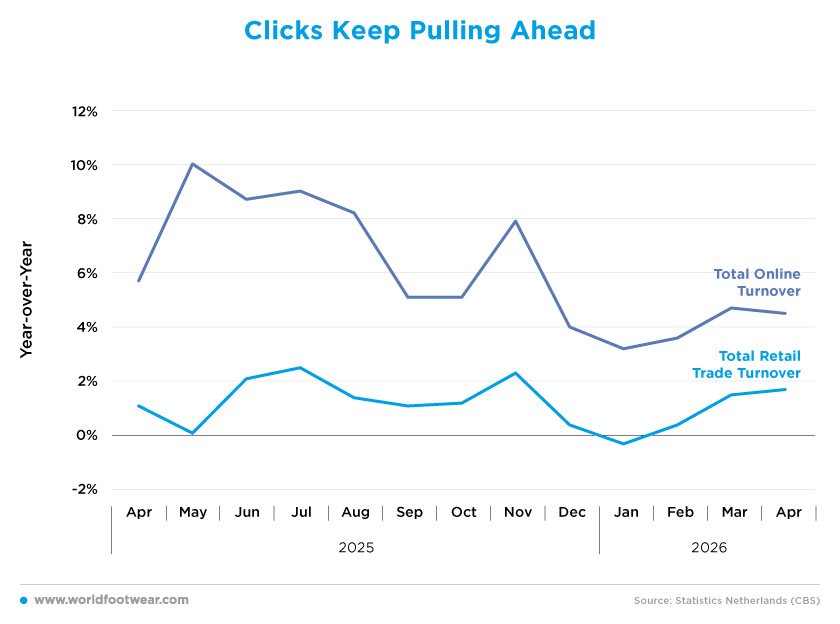

Clicks Keep Pulling Ahead

In volume terms, Dutch retail activity remained positive but modest, while online retail continued to expand at a much faster pace. This highlights a clear gap between overall retail volumes and the online channel.Total retail trade volume increased in most months, but growth was generally limited. It rose by 1.1% in April 2025 and remained positive throughout most of the period, reaching 2.5% in July and 2.3% in November. However, growth slowed at the end of 2025, with a volume increase of only 0.4% in December, before turning negative briefly in January 2026 (-0.3%). It then recovered gradually, reaching 1.7% in April 2026.

Meanwhile, online retail showed a much stronger pattern. Online turnover grew by 5.7% in April 2025 and reached double-digit growth of 10.0% in May. Although this growth slowed down afterwards, it remained well above the total retail volume in every month, ending the period with increases of 4.7% in March and 4.5% in April 2026.

Overall, online retail remains structurally stronger than total retail in terms of volume. Fashion and footwear retailers face the dual challenge of capturing online demand and competing in a market where consumers have more digital and cross-border alternatives.