Register to continue reading for free

France Retail: Widespread recovery remains elusive

After an uncertain 2025, the French retail market is showing few signs of widespread recovery. While online sales remain its main source of growth, overall retail has stagnated and the footwear market continues to struggle with subdued consumer demand. Meanwhile, the recent acceleration in headline inflation has not resulted in higher clothing and footwear prices, which suggests weak pricing power and ongoing promotional pressure. Against a backdrop of fragile consumer and retail confidence, it is no surprise that businesses have become more cautious in their approach to inventory management

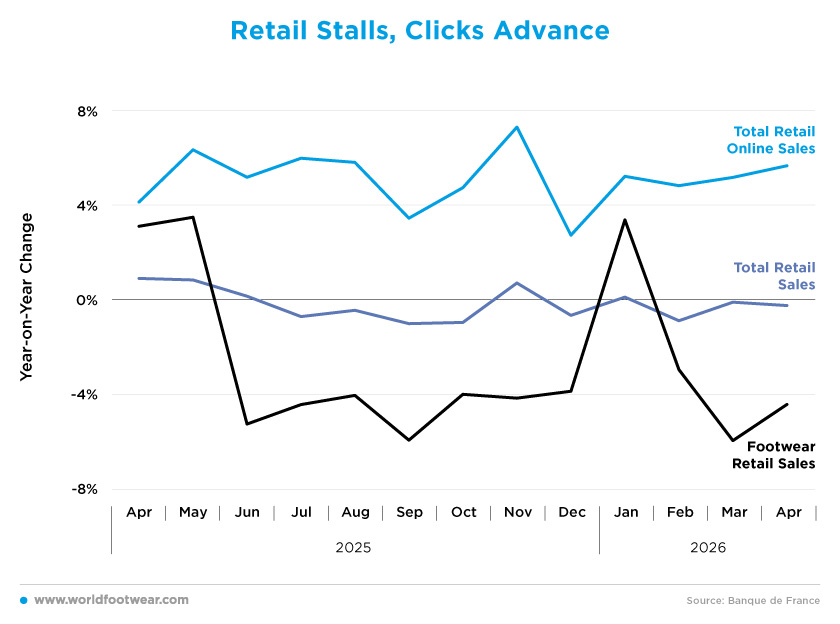

Retail Stalls, Clicks Advance

French retail sales showed little momentum over the analysed period. Total retail sales remained close to flat, fluctuating between modest growth and slight contraction. Following growth in April and May 2025, sales turned negative in the summer and early autumn, before recovering slightly in November. The pattern remained weak in 2026, with total retail sales standing at 0.1% in January, before turning negative again from February onwards and reaching -0.2% in April.Online sales followed a much stronger trajectory. Total online retail sales increased every month, generally growing by between 4% and 6%, peaking at 7.3% in November 2025. This trend continued into 2026, with online sales rising by 5.2% in March and 5.7% in April. While total retail experienced near-stagnation, the online channel remained the clearest source of growth.

Footwear retail sales followed a much weaker path. After growing in April and May 2025, footwear sales fell sharply in June and remained negative for most of the subsequent months. The only clear improvement came in January 2026, when sales increased by 3.4%, but this rebound quickly faded. By March and April, footwear sales had fallen by 5.9% and 4.4%, respectively.

The weakness of the footwear sector should be read in the context of a broader fashion market that remains under pressure. Recent data from the French Fashion Institutes’ Distributors panel shows that clothing and textile sales have struggled to recover fully and remain below pre-pandemic levels, with independent multi-brand retailers being particularly vulnerable (fashionunited.fr). By contrast, digital resilience is also evident in fashion retail. Preliminary figures point to continued growth in online sales, while physical outlets experience lower footfall and lower conversion rates (fashionunited.fr).

Overall, this suggests an increasingly fragmented retail market, with online sales continuing to expand, total retail remaining almost flat, and footwear is struggling to convert demand into sustained growth.

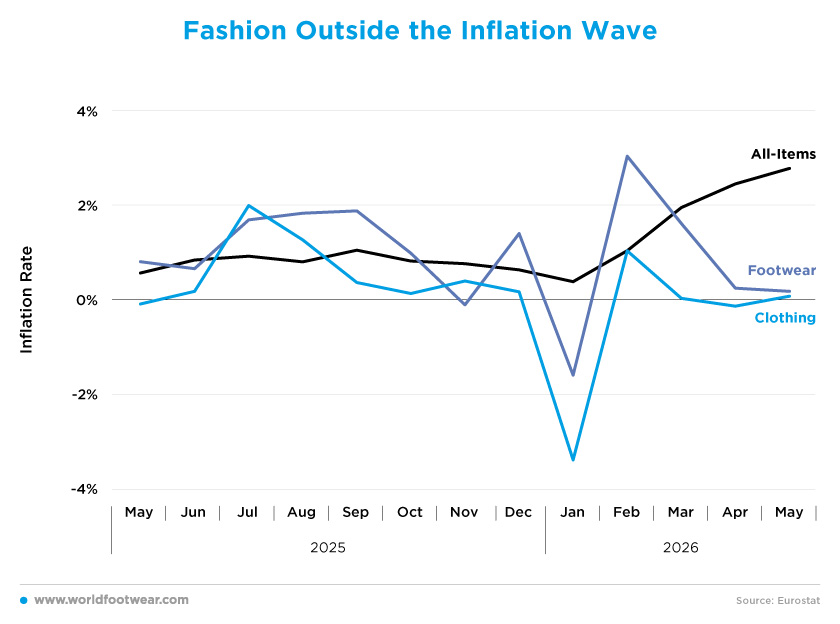

Fashion Outside the Inflation Wave

Inflation in France clearly accelerated in the first months of 2026, while prices of clothing and footwear prices remained much more subdued. This marks a shift from the relatively low inflation environment seen throughout most of 2025.

All-items inflation remained below or close to 1% for much of 2025, fluctuating between 0.6% and 1.1% between May and December. However, this trend changed at the start of 2026. After standing at 0.4% in January, it rose to 1.1% in February, 2.0% in March, 2.5% in April and finally reached 2.8% in May. This brought French inflation to its highest level in more than two years, confirming that price pressures had strengthened following the relatively subdued levels recorded earlier in the period (reuters.com).

However, clothing prices remained weak. After modest increases throughout most of 2025, clothing inflation plummeted in January 2026, reaching -3.4%. It recovered in February, but remained close to zero thereafter, at 0.1% in March, -0.1% in April, and 0.1% in May. Footwear prices also fluctuated considerably. Prices increased during parts of 2025, reaching 1.9% in August and September, before falling by 0.1% in November. In 2026, footwear inflation dropped to -1.6% in January, rebounded sharply to 3.1% in February, and then slowed again to 0.2% by May.

This divergence is consistent with signs that new inflationary pressures are not yet spreading evenly across the consumer economy. According to an analysis by Stéphane Colliac from BNP Paribas, higher energy and input costs resulting from current geopolitical conflicts are beginning to impact parts of the production chain, particularly intermediate goods. Still, inflationary pressures on consumer goods and services remain more moderate. Some firms may also absorb part of the cost increase through margins, particularly in a context of weak demand (economic-research.bnpparibas.com).

This seems to be the case for the fashion sector, which may be also affected by cautious spending behaviour due to economic uncertainty. Therefore, the main message is not that fashion prices are driving inflation, but rather the opposite: while headline inflation is rising, clothing and footwear prices remain comparatively contained. This may be due to weak demand, promotional pressure, and limited pricing power within the sector.

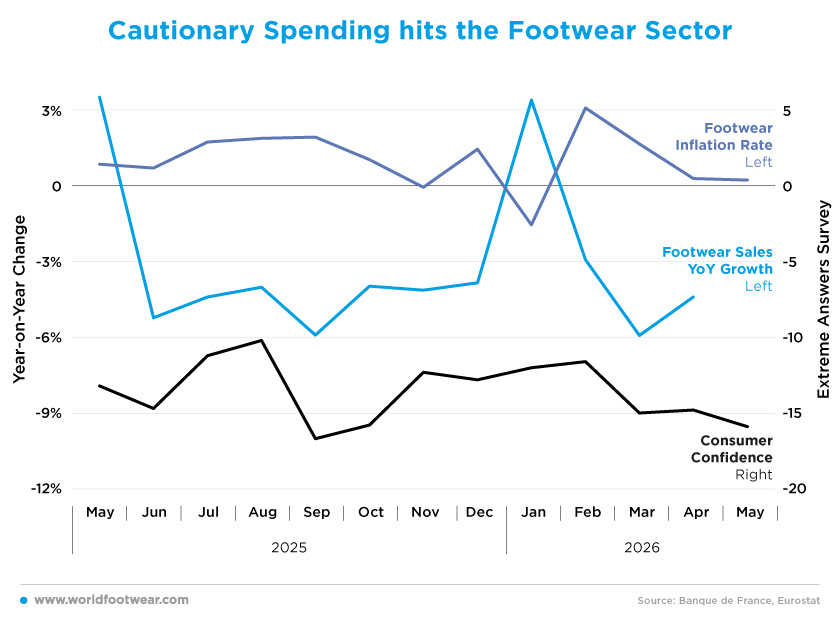

Cautionary Spending hits the Footwear Sector

The footwear sector remained under pressure for most of the analysed period. Following positive sales growth in May 2025, footwear sales turned negative in June and remained in decline for the remainder of the year. The only clear exception was in January 2026, when sales increased by 3.4%. However, this improvement was short-lived, with sales falling again in February, March and April.Consumer confidence provides useful context for the footwear sector’s weakness presented in the first two sections.

Although the indicator does not specifically refer to footwear consumers, it remained negative throughout the period, deteriorating notably in September 2025 and again in March, April and May 2026. This suggests that footwear sales were taking place in an environment of broader household caution, with consumers becoming more concerned about their personal financial situation, unemployment and past inflation (reuters.com).

The evolution of footwear inflation presented does not point to strong pricing power in the sector and aligns with a general pattern of cautious discretionary spending. According to recent reports, non-essential categories remain under pressure, with households adopting a wait-and-see approach and fashion retailers facing weak demand, lower footfall and shrinking profit margins (fashionunited.fr).

This graph illustrates the state of the footwear industry: weak sales are occurring alongside persistently negative consumer confidence and only limited price growth for footwear. This suggests that the problem in this sector is less to do with rising prices and more to do with fragile demand and limited willingness to spend.

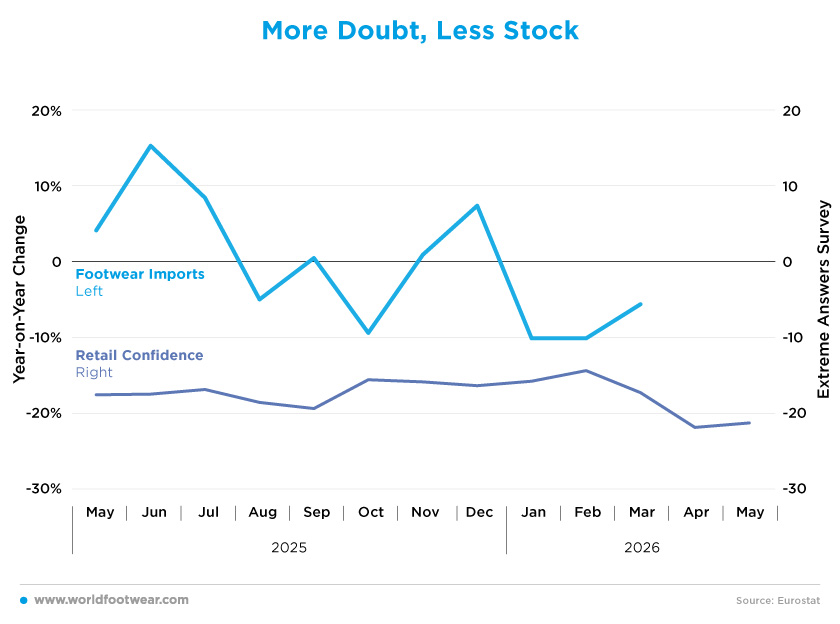

More Doubt, Less Stock

Over the analysed period, footwear imports into France showed a clear loss of momentum. Following a 4.2% increase in May 2025, imports grew significantly in June and July, at 15.3% and 8.5%, respectively. However, this momentum faded from the summer onwards. Imports fell by 4.9% in August, by 9.3% in October, and then contracted sharply at the start of 2026, with further declines of 10.0% in both January and February and 5.5% in March.Retail confidence remained deeply negative throughout this period. The indicator stood at -17.5 in May 2025 and remained in negative territory for the rest of the year, reaching a low of -19.3 in September. Although there was some improvement at the start of 2026, with confidence reaching -14.3 in February, this was only temporary. By April and May, retail confidence had deteriorated sharply again, falling to -21.8 and -21.2, respectively.

This deterioration reflects the challenging business environment for French retailers, as discussed in the previous sections. Weak consumer demand, uncertainty over inflation, and pressure on non-essential spending are all weighing on activity.

The decline in imports at the start of 2026 therefore appears to be a consequence of a more cautious approach to stock management. With retail confidence weakening and footwear sales already under pressure, importers may be limiting their exposure to unsold inventory rather than anticipating a strong recovery in demand.

As import data only goes up to March, it is not yet possible to assess whether the sharp fall in retail confidence in April and May led to a further contraction in footwear imports.